StellarFi

Strengths

- May improve your credit score within the first few months

- Reports to the major credit bureaus

- No hidden fees, deposits, or interest charges

- Access to free financial and credit education

Weaknesses

- No free plan

- Limited customer service availability

- Doesn’t report past payments before enrollment

- Still a young company

StellarFi is a credit builder platform that doesn’t require you to borrow money, pay interest, or make any security deposits. Instead, it converts your regular monthly bills into a powerful credit-building tool.

But how does StellarFi compare to the many credit-building products available on the market, and does it really work? In this StellarFi review, we’ll explain how the platform works, how much it costs, and how it can help you build credit.

Table of Contents

What Is StellarFi?

StellarFi is a credit-building service that opened to the public in July 2022. According to the financial technology (fintech) platform, over 130 million Americans don’t have access to a homeownership path or a financial safety net to afford emergencies.

One of StellarFi’s key selling points is that it allows you to build credit without a credit card by reporting your monthly payments to two of the major credit bureaus (Equifax and Experian). Furthermore, you won’t undergo a hard credit check which can impact credit decisions for the next two years.

How StellarFi Works

Getting started with StellarFi is easy. You simply connect your monthly bills to a StellarFi Bill Pay Card, which acts like a line of credit. This credit line pays your bills and immediately draws the funds from a linked bank account, so you never carry a balance or pay credit card interest.

StellarFi has been adding additional perks as its customer base expands. This includes bill payment rewards and other perks on its upper-tier plans.

Let’s take a closer look at how you can bolster your credit score.

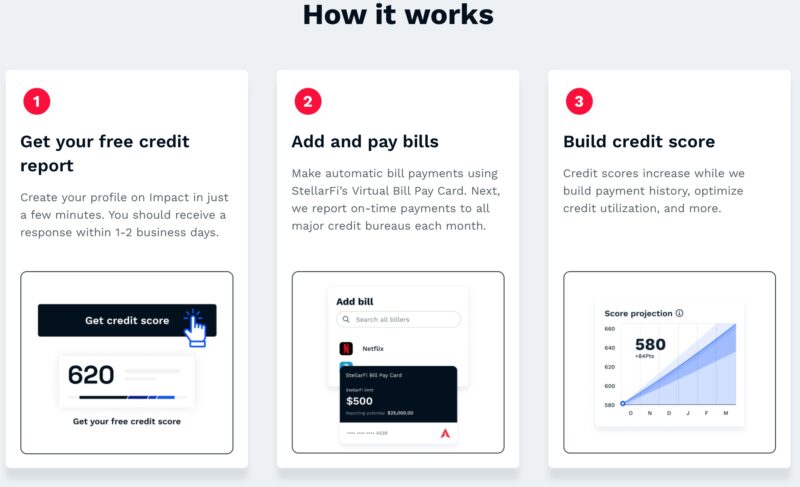

Free Credit Report

You can check your credit score for free after creating your StellarFi profile (there is no impact on your credit.) This provides a baseline from which to track your progress with each bill payment.

Your StellarFi credit score is a Vantage 3.0 scoring model from the three bureaus. Most credit score apps only monitor one or two scores.

One minor frustration is that you see a Vantage 3.0 credit score instead of a FICO Score, which is the most common credit score. The FICO Score is the one the lenders use when they perform a credit check. So, the VantageScore isn’t as precise, but you have a firm idea of your current credit score range.

Add and Pay Bills

After completing the initial account setup, you can link your recurring monthly bills, such as your cable TV, internet, or phone bill. You receive a virtual StellarFi payment card that you can provide the biller to pay the monthly tab.

StellarFI’s auto-connect feature lets you quickly update your payment method with most national brands. You can also link bills manually with merchants that StellarFi doesn’t have a direct relationship with.

In addition to linking bills, you connect your checking account to StellarFi to pay bills. There are no additional fees to use this service, such as payment processing fees or bank transfer fees. When a bill is due, StellarFi will check your bank to ensure there are sufficient funds to pay the bill to avoid causing an overdraft. If there aren’t sufficient funds, the bill will not be paid. If, for some reason, an overdraft does occur, StellarFi won’t charge overdraft fees, but your primary bank may.

Improve Your Credit Score

By paying your bills through StellerFi, you establish a positive payment history, as you would with a credit builder loan. Even though you’re not borrowing money or buying on credit, it appears as a monthly loan repayment.

Your monthly payments report to two of the major credit bureaus:

- Equifax

- Experian

This extensive reporting is similar to the free service offered by Experian Boost. However, Boost only improves your Experian credit score. It won’t help you build credit with Equifax or TransUnion.

You may notice a temporary drop in your credit score when you first join StellarFi, as the line of credit appears as a new account on your credit reports. A brand-new credit account negatively impacts your average length of credit history (15% of your total credit score) and new credit factors (10% of your total score).

You can get similar results to StellarFi by paying your bills with a secured or unsecured credit card. However, a credit card isn’t ideal if it encourages you to overspend or you end up paying high credit card interest rates. It also will not immediately take the money out of your checking account when you pay a bill.

It can also be difficult to qualify for a credit card if you have bad or fair credit.

Other StellarFi credit-building tools include:

- Creating customized credit goals

- Credit score simulator

- Debt-to-income (DTI) calculator

- Dynamic score projections

✨ Related: How to Increase Your Credit Score

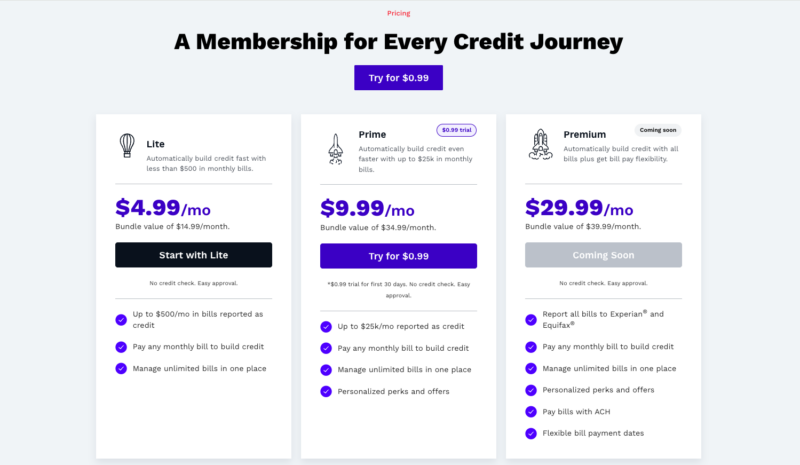

StellarFi Pricing

StellarFi offers three paid plans (there is no free version.) You can upgrade to a higher plan to access a higher credit limit, which may help you minimize your credit utilization ratio and allow you to pay more bills. Here’s a closer look at what each plan has to offer.

Lite

The entry-level Lite plan costs $4.99 monthly and allows you to report up to $500 of bills as credit. Your initial line is smaller until you complete your first bill payment before it expands to $500.

With Lite, you also get access to other essential StellarFI features, including bill pay auto-withdrawal, bill payment notifications, credit score monitoring and alerts, 1-on-1 live credit coaching, and more.

Prime

StellarFi’s mid-tier plan is called Prime, and it costs $9.99 monthly after a $0.99 trial for the first 30 days.

You can have up to $25,000 in bills reported as credit, a significant increase over the Lite plan.

Premium

StellarFi Premium is the highest-tier plan and costs $29.99 monthly. As of January 30, 2024, it is yet to go live – there is a ‘Coming Soon’ notice on the StellarFI website.

According to StellarFi, the Premium plan will include the following exclusive benefits:

- Paying with ACH transfers (as some merchants don’t accept card payments)

- Flexible bill payment dates (Pay bills early and repay StellarFi within 60 days interest-free)

- Identity protection system (SSN monitoring, ID theft insurance and restoration, credit report dispute, and more)

Is StellarFi Safe?

StellarFi uses bank-level 256 AES security to encrypt your personal data. The platform also uses randomized digital tokens and never stores your financial information.

With that said, tech glitches do occur, and there are times when bill payments may not be completed as scheduled. If that happens, StellarFi will make it right by reimbursing any late fees and protecting your privacy.

Remember that StellarFi is a young company, so you must be comfortable dealing with a startup.

Does StellarFi Actually Work?

You can benefit the most from StellarFi if you have a credit score in the low 600s or below. Here are some reported results from StellarFi users on Trustpilot:

- Adrian N. reported an average 40-point increase after the first month

- Angel M. reported an average 45-point increase over 4-6 months.

- Caitlynn D. reported a 20+ points boost during the first 30 months.

- Destany B. reported a 28-point increase after the first month and zero points after the second month before leaving their review.

Keep in mind that these are online reviewers, and their results cannot be substantiated.

Also, from Trustpilot, the most common StellarFi complaints tend to surround a lack of customer service options. Several reviews indicate that chatbots handle the initial inquiry process, and it can be difficult to reach a human.

Ultimately, you can’t rely on StellarFi alone to strengthen your credit history. You must also focus on paying your existing loans and credit cards on time, avoiding opening new credit cards or loans, and keeping existing credit card accounts open as long as possible to have the maximum benefits.

Pros & Cons

We’ve identified the following strengths and weaknesses of StellarFi’s service offering:

Pros

- You can improve your credit score within the first few months

- Reports to all three credit bureaus

- No hidden fees or interest charges

- Can earn cash rewards on bill payments (Plus and Premium plans)

Cons

- No free plan

- Limited customer service availability

- Doesn’t report past payments before enrollment

- Still a young company

Alternatives to StellarFi

Before signing up with StellarFi, it’s a good idea to explore other credit builder platforms. With that in mind, here are a few StellarFi alternatives worth considering.

Kikoff

Kikoff is a credit-building platform that offers a credit account as well as a secured credit card. The Kickoff Credit Account is a $750 credit line. Instead of paying bills, you can buy financial education products, and your payment activity reports to the three bureaus.

Two additional tools include a secured credit card and a credit builder loan. There is a flat, $5 monthly fee for Kickoff’s Credit Service, but unlike some competitors, it doesn’t charge any fees for its secured card or credit builder loan product.

Kikoff review for more.

CreditStrong

You can improve your personal or business credit through CreditStrong. Several credit builder loan tiers are available depending on how aggressively you want to increase your score and your monthly budget.

Check out our CreditStrong review to compare credit-building plans.

Self

Self lets you deposit monthly payments into an FDIC-insured certificate of deposit (CD). The credit builder loan’s repayment term is as long as 24 months with a monthly commitment between $24 and $150. Each payment reports to the three major bureaus, and you are reimbursed the contribution amount at the maturity date, excluding fees.

Additional products include a secured credit card and free rent reporting.

Read our Self Credit Builder review to find out more.

FAQs

No hard credit check is necessary to apply as you only need a Social Security number or individual taxpayer identification number (ITIN) to report payments to your credit bureaus.

Your StellarFi account appears as a revolving line of credit similar to a credit card. Each month, the platform reports your monthly bill payment amount and compares it against your total limit to calculate a credit utilization ratio.

You can pause or cancel your account by accessing the “manage account” button in the personal information menu. Pausing your account keeps your line open to prevent an account closure from appearing on your credit report, but it no longer reports monthly payments as you’re not paying a membership fee anymore.

Chat and email support is available from 8 a.m. to 6 p.m. Central from Monday to Friday. Live phone support is unavailable unless the platform contacts you to schedule a call.

Is StellarFi Worth It?

StellarFi is worth considering if you’re looking for a way to build or repair your credit without a secured credit card or other credit product. One of the biggest advantages of using StellarFi is that it helps you automate your finances and report your bill payments to two major credit bureaus, Experian and Equifax.

Just be mindful of the fees – unfortunately, StellarFi does not offer a free tier – and be realistic about how much StellarFi can boost your credit score. Remember that you will have to stick to sound credit-building practices, such as timely credit payments and regular budgeting, to stay on track for financial success.