EveryDollar

129.99 USDStrengths

- iOS / Android app

- Simple clean interface

- 14-day trial

Weaknesses

- No free version anymore, must pay for Ramsey+

- Must pay for automatic transaction downloads

- May be too simplistic (but does it well)

- No community

If you want to get better at managing your money, you should start with a budget.

But who wants to track everything in a spreadsheet?

(if you do, here are a few free budgeting spreadsheet templates to get you started!)

That’s where a budgeting app comes in.

One of the more well-known apps in this space is EveryDollar. EveryDollar is the budgeting app built by Ramsey Solutions (formerly Lampo Group) and part of Ramsey+. Ramsey Solutions is the organization behind Dave Ramsey, the personal finance media personality.

EveryDollar once offered a free version, where you had to manually enter in transactions, but that has gone away with the introduction of Ramsey+, which is EveryDollar Plus and a suite of financial courses.

EveryDollar relies on his money principles, known as the Dave Ramsey Baby Steps, and the debt snowball repayment technique.

Dave Ramsey can be a polarizing figure but so many have used his approach to get out of debt. I’ve talked to people who used his books to get their financial life in order.

The results speak for themselves. You don’t have to agree with his personal and political views if you want to use his personal finance approach.

Let’s see how EveryDollar works:

Table of Contents

How Does It Work?

EveryDollar uses the budgeting system known as zero-based budgeting. In zero-based budgeting, you assigned every dollar to a category. It’s very similar to envelope budgeting.

This is where you input your monthly income and plan your entire month’s spending ahead of time. You set up budgeting categories and then allocate your income to those categories.

Then you use the app to track your spending daily. If you have the free app, you manually enter your transactions. If you pay for EveryDollar Plus, you can link accounts and it’ll automatically pull in transaction data. It’s a very popular alternative to Quicken.

Setting Up EveryDollar

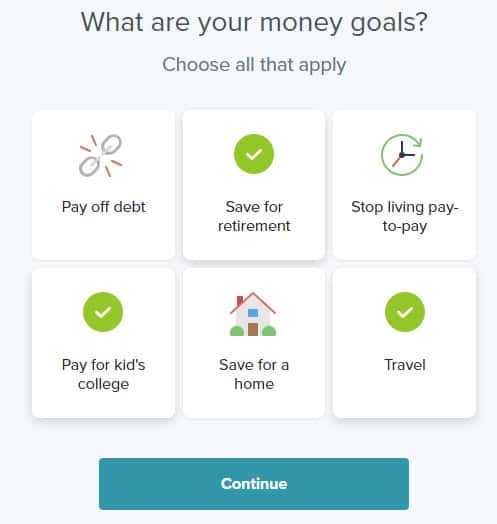

Signing up is easy. After you register, you’re asked to pick one or more money goals:

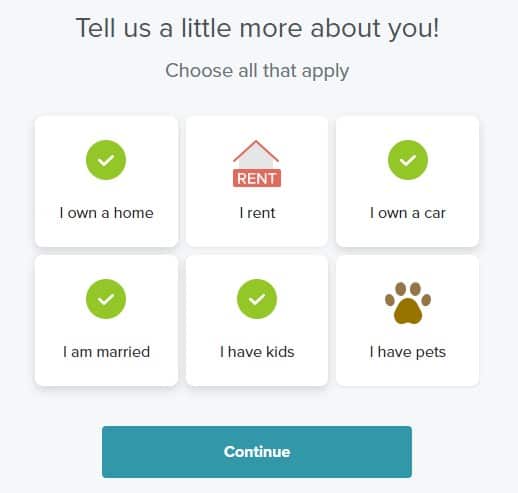

Next, you’re asked for some more personalized information:

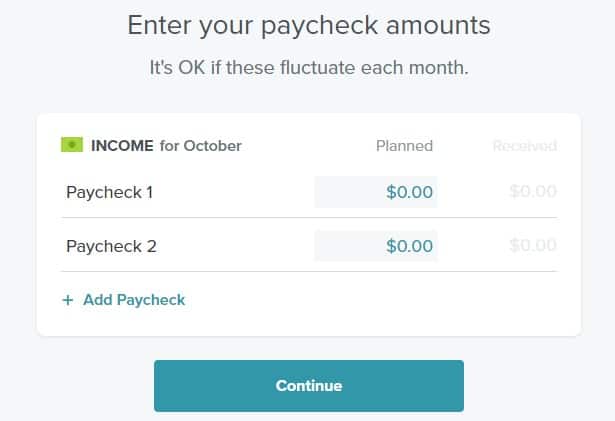

The setup process continues with you entering your income, expenses, giving, and debt figures.

Here’s what the income section looks like:

If you are paid every two weeks, you can set the income to be your total in a month or set two (or three depending on the month) line items for the two pay cycles.

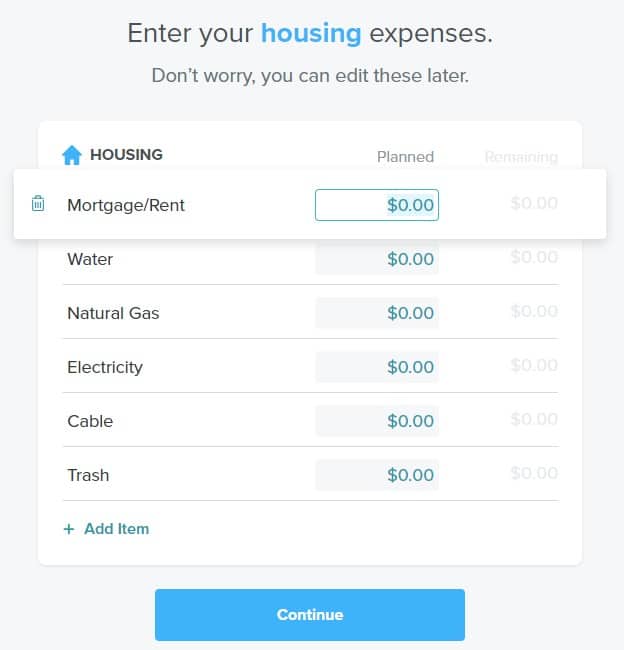

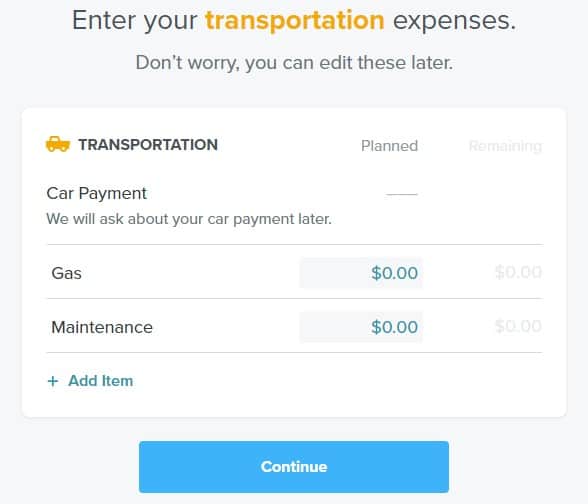

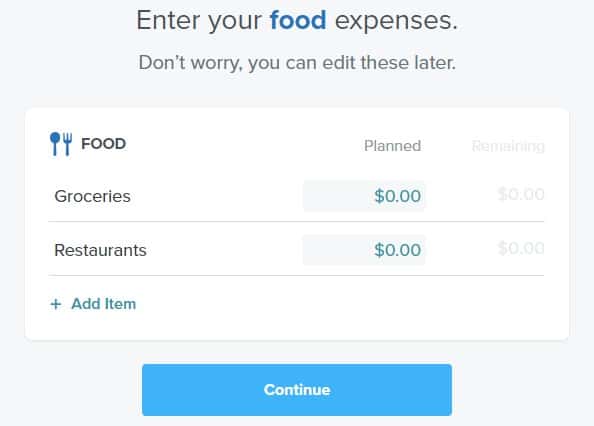

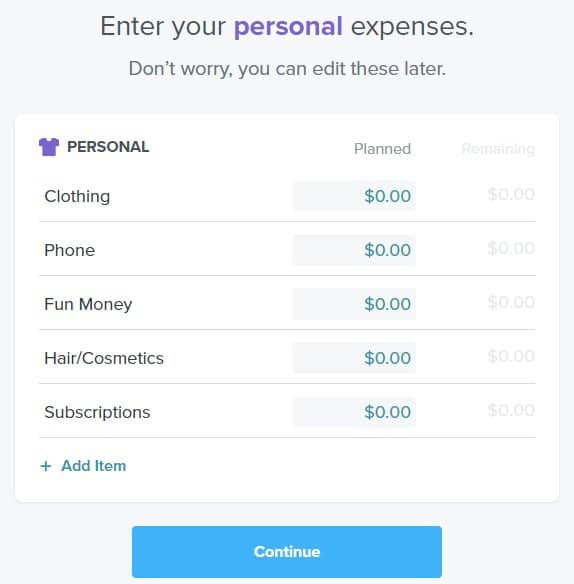

Then you’ll enter your basic expenses (housing, utilities, food, transportation and “personal expenses”):

You can edit the names of the line items and add new items to each list. Throughout the process, you can review how well you’re allocating your income.

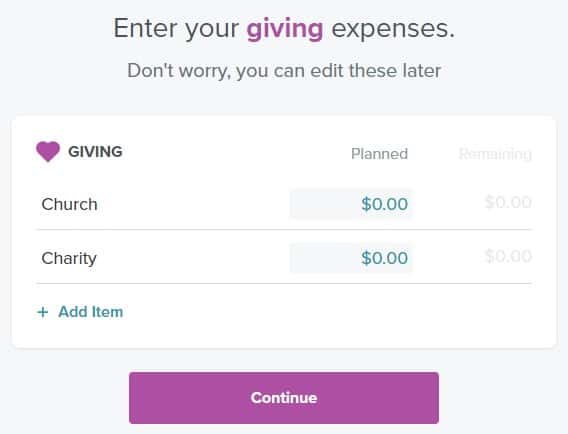

Next, you allocate charitable giving:

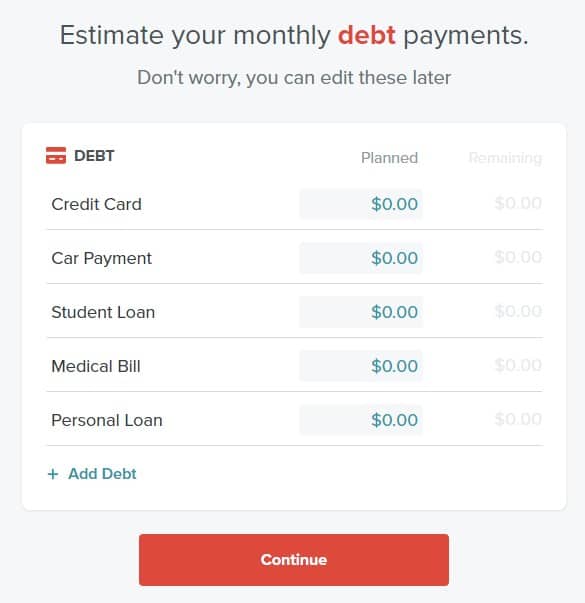

Finally, the coup de grace, you have debt payments:

Note: You’re supposed to enter the monthly payments, not the amount of debt owed. You will notice that your mortgage payment, while technically a debt payment, is NOT included in this list.

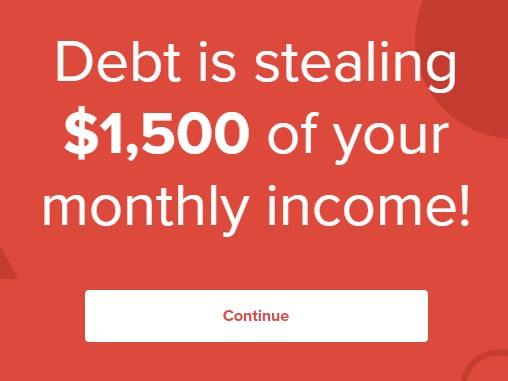

This is what EveryDollar says after you enter in your debts:

Intense!

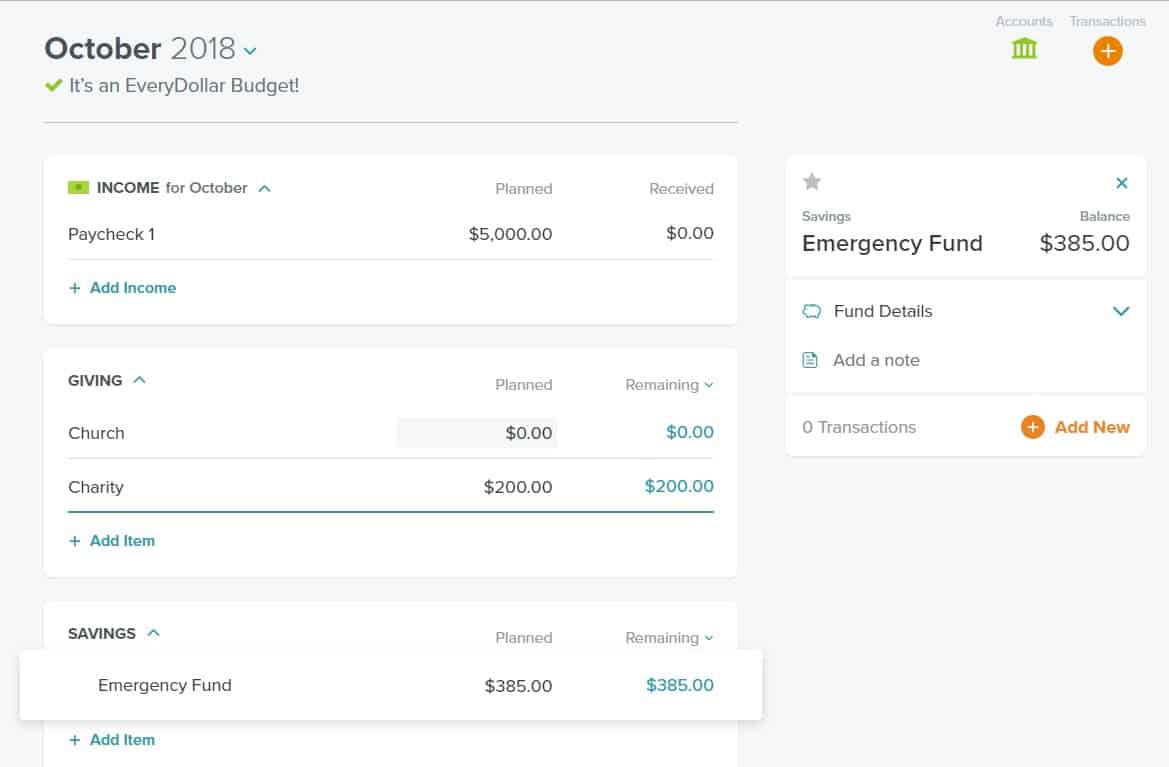

Since debt payment is the last expense to enter, you’ll have a surplus or a deficit. The quickest way to get this in balance is to put that surplus into a savings category on the dashboard:

You’ll notice the Savings line item called Emergency Fund has a planned $385.00 figure. When this happens, the text underneath the Month and Year will say: “It’s an EveryDollar Budget!”

Adding Transactions

Up until now, you were setting your planned spending amounts. You don’t track actual earning and spending until you add transactions.

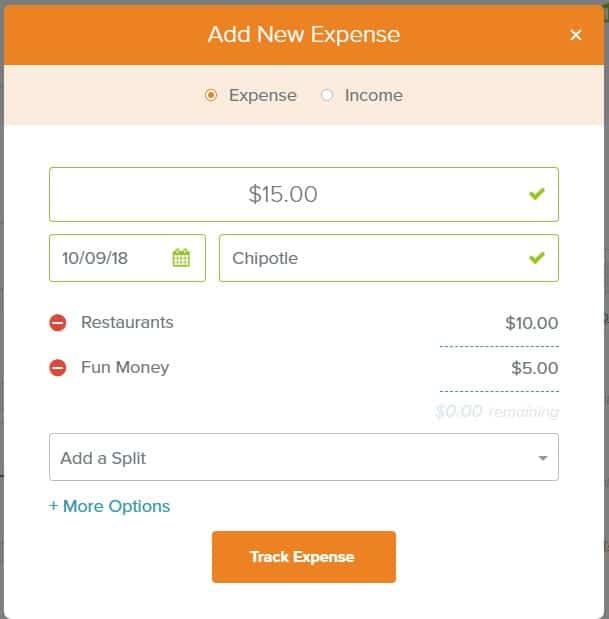

You can add an income or expense transaction, the screen above shows an expense at Chipotle for $15. You can split the transaction across many categories. I showed it split across Restaurants and Fun Money.

If you click on more options, you can add a Check # as well as Notes.

If you switch the transaction type to income, the options don’t change. The only difference is the button changes to “Track Income” instead of “Track Expense”.

On the dashboard, bars will show your progress:

Including the Baby Steps

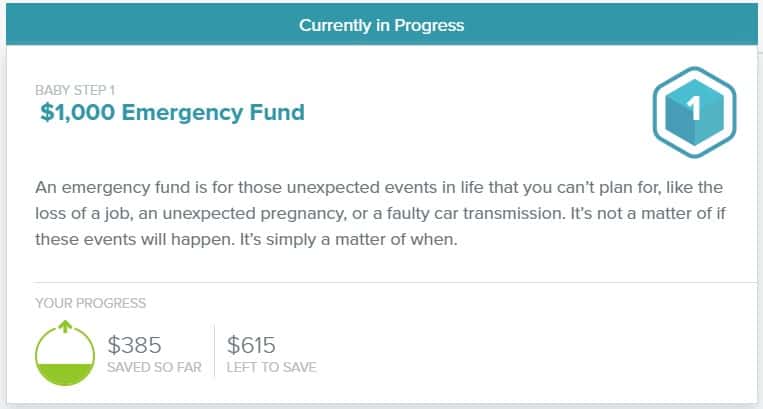

Dave Ramsey is well known for his Baby Steps, a set of seven money “steps” that he has shared for decades.

There’s a section that talks about those steps and tracks your progress. Here’s the box for the first step, saving a $1,000 Emergency Fund.

What is a little confusing is that the $385 “saved so far” is a misnomer. That was only what I had planned to save in October, I haven’t added a transaction showing I “saved” that amount.

If I add an expense transaction and allocate it to the Emergency Fund savings, the amount drops to $0. EveryDollar treats the emergency fund savings line item as an expense, like clothing or restaurants.

It seems like to “save” that, I have to have income left at the end of the month and then it assumes I save it there.

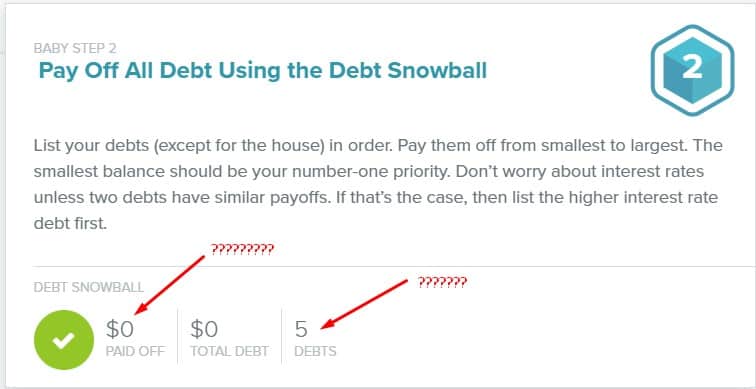

I was also confused by Baby Step 2 as “complete” because I listed several debts:

The budget isn’t debt-free… so why is EveryDollar saying everything is OK?

EveryDollar Alternatives

EveryDollar offers zero-based budgeting but not much more, so if you want a different budgeting strategy, EveryDollar isn’t the best choice.

Also, EveryDollar doesn’t track investments or have a community to join. For any of those, you’ll need an alternative. Check out these suggestions below, or our list of the best budgeting apps for couples.

You Need a Budget

The closest alternative to EveryDollar is You Need a Budget, or YNAB. YNAB is a zero-based budget “give every dollar a job” system that costs $6.99 per month (with a 34-day trial) and is cheaper than EveryDollar.

In a YNAB vs. EveryDollar comparison, YNAB has a slightly bigger learning curve but the tool and the support are way better. One of the biggest assets of YNAB is the community of people who use it. You can get a ton of support from the company but also other people like you.

Empower

Empower has automatic transaction downloads to a budgeting tool that does basic expense tracking and budgeting. Empower is not on par with similar budgeting tools but they do investment tracking, which isn’t available in EveryDollar and others on this list.

As your finances evolve beyond budgeting, you’ll want an eye towards the future and your retirement. Empower offers those tools for free and is a good way to help ensure your investments perform the way you need them to.

The Bottom Line on EveryDollar

If you’re a fan of Dave Ramsey and his approach to money management, EveryDollar is an intuitive and easy-to-use tool to help you manage your money. The interface is also very clean and doesn’t appear to have advertisements.

If you’re just looking for a budgeting tool, it’s hard to justify paying $130 a year for a budgeting tool like this one. When you lay in the educational component, it makes a little more sense but I’d argue your money is better off spent on necessities rather than a budget. There are many great budgeting tools available for free (or ad-supported) so you can keep the $130 to go towards something else.

If you’re interested in the Ramsey Pros or the financial education, it might be worth it. That’s really up to you to decide.

Interesting review. I’ve always heard Dave Ramsey referencing Every Dollar, but I’ve never actually taken a look. Great review. Now, I know a little bit more about the app and I must admit it sounds intriguing. Since it’s free it might be worth a try. This is especially true since I loosely follow Dave Ramsey’s principles (emphasis on loosely).

It’s a very straightforward budgeting app, not too many bells and whistles to it.

I’ve been using Goodbudget for several years. A true envelope system. You do have to manually enter your transactions (or import from your bank), but that’s the only drawback. And, yes, you can reconcile your bank statement!

Why it is never included in reviews, I don’t understand. It’s a great product.