Empower Personal Dashboard FREE

Product Name: Empower Personal Dashboard

Product Description: Empower Personal Dashboard is a free personal finance tool that can collect your financial data into one easy to read dashboard. They offer a rich set of features to help you build wealth, plan for the future, and can put you in touch with wealth advisors if that's something you're interested in (if you aren't, make sure you let them know because they are persistent).

About Empower

Empower is a financial services company that primarily offers retirement plan recordkeeping. They are based out of Colorado and the second largest retirement plan provider in the United States. Founded in 1891, they have over a trillion in assets under management.

Overall

-

Features

-

Ease of Use

-

Fees

-

Customer Service

Pros

Easy to set up

Rich investment analysis tools

Intuitive design and user interface

Cons

Budgeting tool needs improvement

No historical data (can’t import either)

Want to know how Empower Personal Dashboard (formerly Personal Capital) helped me manage all of my money, including investments, in only a few minutes a month? You’re in the right place.

When I first started managing my money, I did everything manually in a spreadsheet.

Every month, I’d log in to each of my accounts and record the balance in my Net Worth Record. I’d go into my bank accounts, my investment accounts, my mutual fund account, my credit card accounts…

It would take me an entire hour to get every account. It was so bad that I started consolidating and closing accounts just to shorten the process.

For a very brief moment, many years ago, I tried Quicken and subsequently Mint. They were all OK — but they didn’t do a good job integrating my brokerage accounts. Eventually, I abandoned them and went back to manually logging in. (if you are looking to quit Quicken, keep reading, you’ll see why I list Empower Personal Dashboard as one of the best alternatives to Quicken)

Fast forward to today and I spend just 15 minutes each month managing my money.

Just 15 minutes each month plus another five each week is enough to get everything right… and the cornerstone of that system is a tool called Empower Personal Dashboard.

It’s free, it’s well-designed and what started as a test run has become my permanent solution (it’s my favorite of the Mint alternatives).

I use Empower as a way to quickly collect brokerage investing and banking data for my Net Worth Record, a spreadsheet I use to track our family’s net worth. Empower will pull the data from each account so I don’t need to manually log in. It separates itself from other services because the investment management portion is not an afterthought and fully integrated into the system.

Many other tools started as a budgeting tool that added on an investment component. Empower started as an investment tool that added in budgeting.

Table of Contents

- About Empower Personal Dashboard

- The Sign Up Process

- Transactions

- Portfolio Tracking

- Tracking Other Non-Investment Assets

- Complimentary Portfolio Review

- Other Free Tools

- Retirement Planner

- Financial Roadmap

- Empower Personal Cash

- Additional Services

- Smart Withdrawal

- Empower Fees

- Empower vs. Mint: Is Empower better than Mint?

- Is Empower Personal Dashboard Safe?

- What Needs Work?

- Final Word

🔃Updated December 2023 to update the screenshots, which largely remained the same except for a new logo and new fonts. Nothing changed about the tools themselves.

About Empower Personal Dashboard

Personal Capital was founded in mid-2009 with the mission of “better financial lives through technology and people.” In 2020, they were acquired by Empower, which is the second largest retirement provider in the United States. In February of 2023, they were rebranded from Personal Capital to Empower Personal Dashboard.

❓What happened to Personal Capital? Personal Capital was acquired by Empower Retirement in 2020 and in February 2023, it was re-branded into Empower Personal Dashboard. Everything about the tools remained the same except for a new logo and name. You can read more about what happened to Personal Capital in this post.

As of March 2022, they serve 3.3+ million registered users (I am one of them!) and manage over $23.2 billion in assets for over 31,800 clients (that’s what pays for the service, fees on those managed investment assets) – that’s some serious cash.

The business has two components: a free personal finance aggregation tool and a paid advisory service. This review will look only at the aggregation tool side as I haven’t used the paid advisory service.

Located in California, it was founded by Rob Foregger, Bill Harris, and Louis Gasparini. Bill Harris was the CEO of Persona Capital and was formerly CEO of Intuit, Paypal, and several other financial services and security companies.

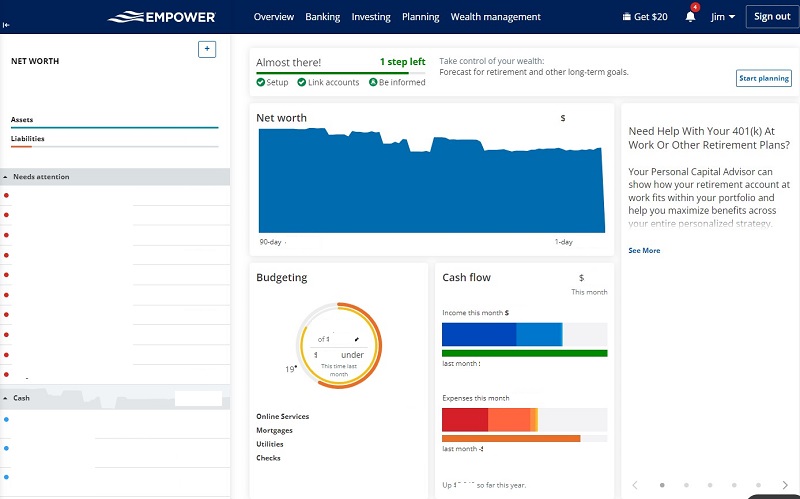

The Sign Up Process

Signing up was fast and they had every one of my accounts available for linking, including my Maryland 529 plans. Take that Quicken!

Transactions

The Transactions menu item is where you’ll find the budgeting tools that were the newest addition to Empower Personal Dashboard. If you’ve used Mint or other budgeting tools, it’ll look familiar.

You have a list of transactions categorized into Income and Spending, followed by Bills.

Here’s a shot of the All Income Cash Flow chart:

Like any tool, there are a few hiccups to adjust post-transaction, especially when you transfer between accounts, but it’s a quick adjustment.

Until you do that, you sometimes get wildly crazy numbers. 🙂

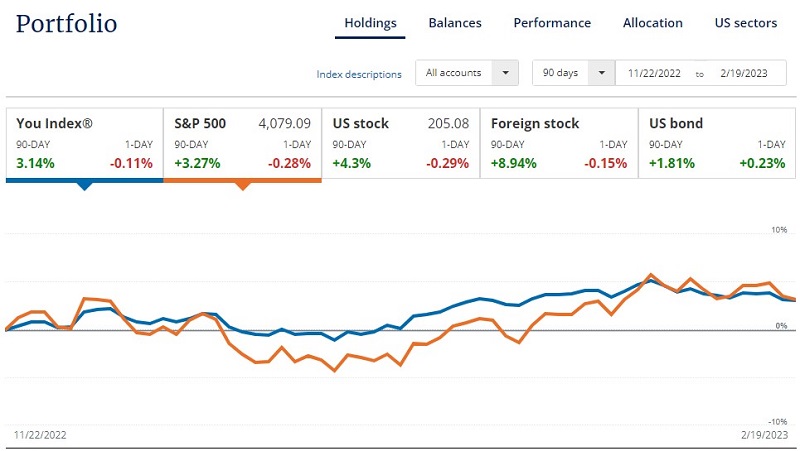

Portfolio Tracking

As I mentioned earlier, Empower Personal Dashboard started on the investment side and only recently added the budgeting toolset… so the portfolio tools are better.

Here’s what I see under Investing -> Holdings:

This snapshot was taken in the morning of February 19th, 2023.

As you can see, we’ve enjoyed a good run for the start of the year.

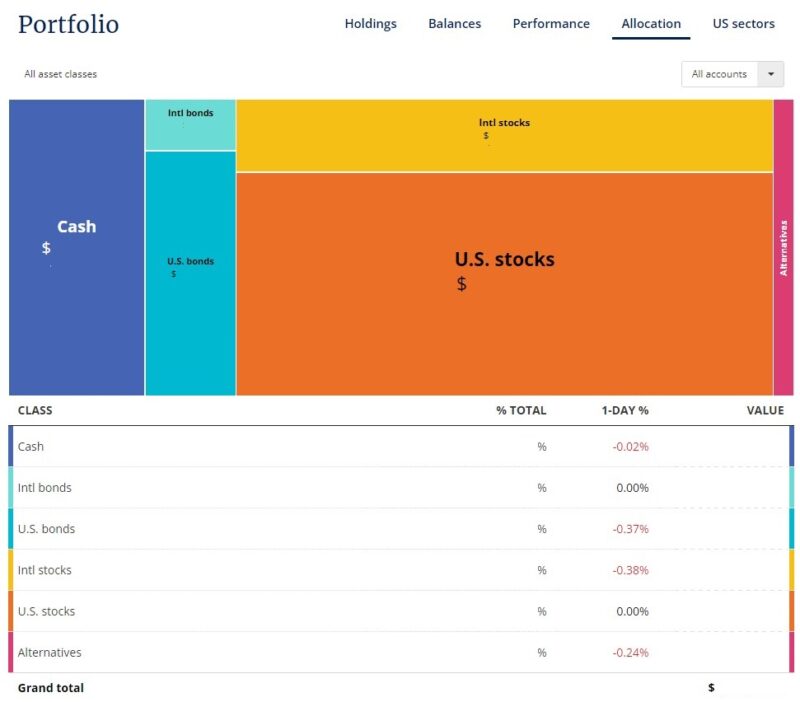

The Balances and Performance tabs are less interesting than the Allocation tab.

Empower pulls this data from all of my brokerage accounts, which right now is just at Vanguard and Ally Invest, and giving me a full breakdown of my allocation. I can click on one of the boxes and it can give me an even granular breakdown:

If you click down one more level, it starts telling you the actual holding and the amounts you have.

The last fun chart we have is US Sectors:

It breaks down your investments based on the sector:

- Basic materials

- Communication services

- Consumer cyclical

- Consumer defensive

- Energy

- Financial services

- Healthcare

- Industrials

- Technology

- Utilities

Can’t Find Your Institution?

If you are having trouble finding your financial institution, Empower may not have added support for them yet. For quite some time, my brokerage wasn’t supported (it is now) but there are workarounds.

First, you can check if perhaps your institution is named something else. The best example is a Fidelity 401(k) – it turns out that it’s run through NetBenefits. If you have a Fidelity 401(k) then you won’t find “Fidelity 401k” in the account listings – it says Fidelity (All accounts except 401k). For an actual Fidelity 401k, you will need the NetBenefits one.

If you work at Textron and want to find your 401k for them, it’s Fidelity NetBenefits Textron. Confusing but at least it’s there!

Next, you can manually add publicly traded securities into a portfolio that Empower will track on your behalf. So previously, I just put in all my holdings. 100 shares of Company Y, 150 shares of Company Z, etc. It’s cumbersome the first time but then it tracks as normal.

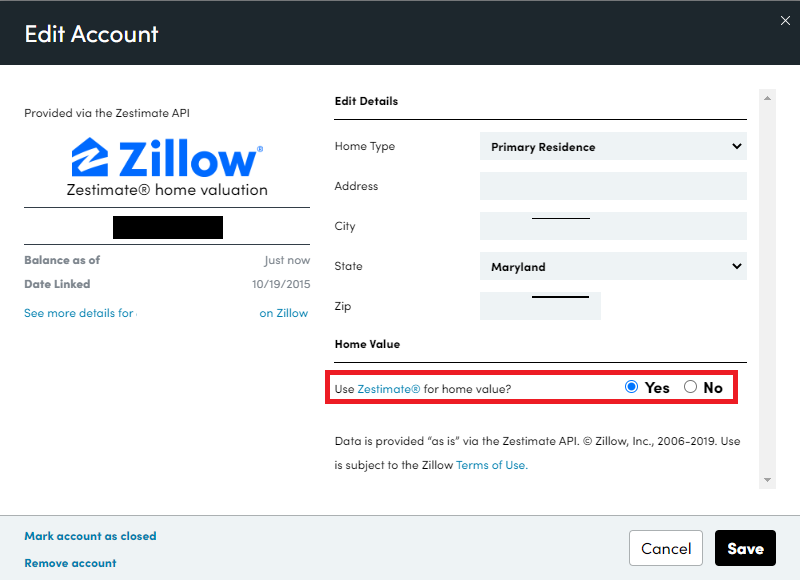

Tracking Other Non-Investment Assets

You can track “other assets” like art, cars, etc – there just isn’t any updating functionality because there’s no central database of pricing for those types of things.

One exception is real estate, which you can track to Zillow’s Zestimate:

I’m not sure how I feel about Zillow’s Zestimates as an accurate measure (here are some other free home appraisal tools) but I set my home’s value at my purchase price because I need something to offset my negative mortgage balance.

For the longest time, the Zillow information for our house was wrong but I didn’t care enough to go through the process of updating it.

I don’t want my perspective on our net worth affected by our home’s “value.” I just assume it has held the value we assigned at purchase. They have a feature where you can tie in a Zillow estimate (Zestimate), but I don’t use it.

If you invest in real estate, for rental or otherwise, I can see the Zestimate is a little more valuable because you’ll be interested in marking it’s value to the market (even if it’s an estimate).

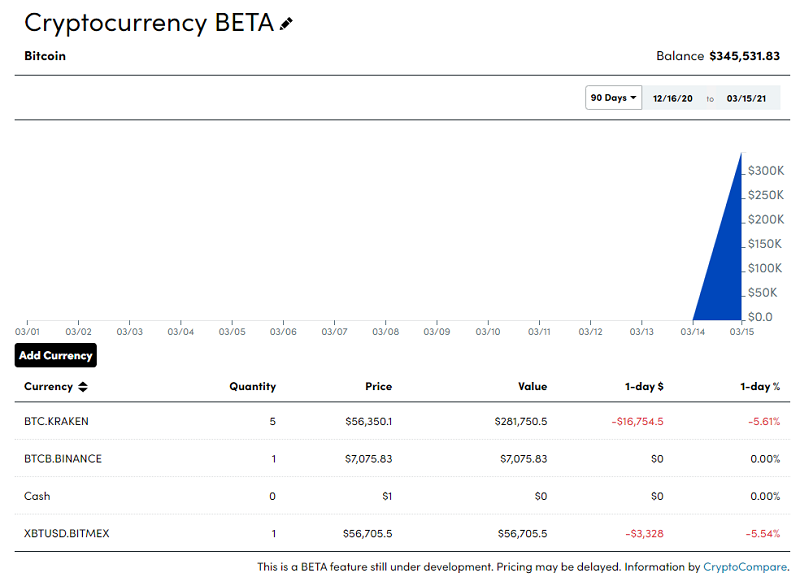

Tracking Cryptocurrency Holdings

Empower also offers the ability to track your cryptocurrency holdings. You can add your cryptocurrency holdings and they will track the pricing based on CryptoCompare.

It’s tracked under “Other Assets” and you manually enter your holdings but the value will be tracked automatically. For example, you select your exchange followed by the currency and the amount you have. I don’t have any so this is all dummy information:

If you have cryptocurrencies, this is a convenient way to integrate them into your dashboard. I don’t think many, if any, other services off this yet.

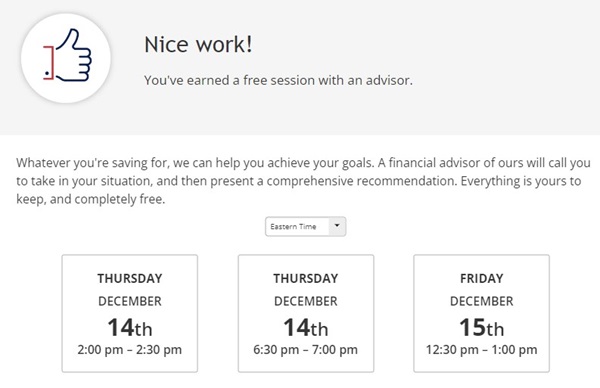

Complimentary Portfolio Review

When you connect $100,000 or more in investable assets, you can get a free portfolio and personal financial review – they value it at $799. It’s complimentary and they take a closer look at your financial situation and can help you figure out if you’re on track to reach your goals.

They can do everything from finding whether you’re overpaying in fees to building a college savings plan, all without any obligation. It’s a fantastic way to get a second look at your situation and see if there are any spots you’re missing.

As you use the tool, you’ll periodically get pitched a free session (I suspect this is only if you’ve linked $100,000 in assets):

Other Free Tools

The free tools section offers the following:

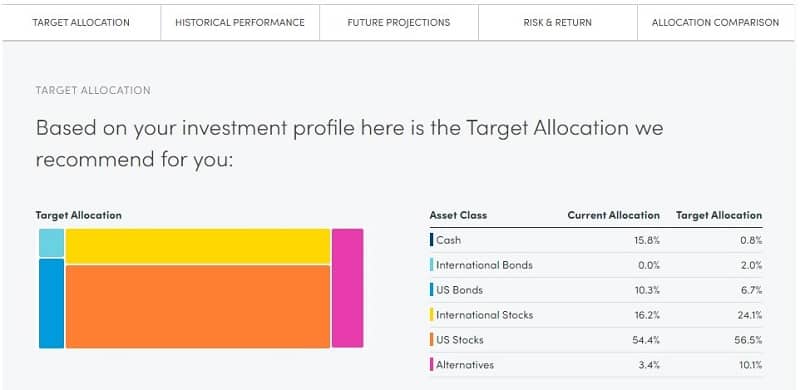

- Investment Checkup: Given what you’ve shared in your enrollment, they would recommend an allocation. I’ll expand on this below.

- Retirement Planner: This looks at whether or not your current pace of savings will be enough to support your retirement. It’s a really fun tool I’ll have to play with some more. (can you tell I’m a forecasting/stats nerd yet?))

- Retirement fee Analyzer: This takes a look at all the expense ratios in your various accounts and tell you if you’re paying too much. The vast majority of our holdings are in Vanguard funds so there’s not much to see here.

- Advisor: This is a page where you can schedule a call with a fee only financial advisor. The fee is an annual fee and based on assets under management.

- The Currency™: The name of their blog.

So more on the Investment Checkup tab, this will take your investment profile and recommend a target allocation. Here’s mine:

Here’s where rebalancing comes into play. If things are out of whack, it’s important to rebalance each year. This is a good reminder.

They also offer an Advisory Service:

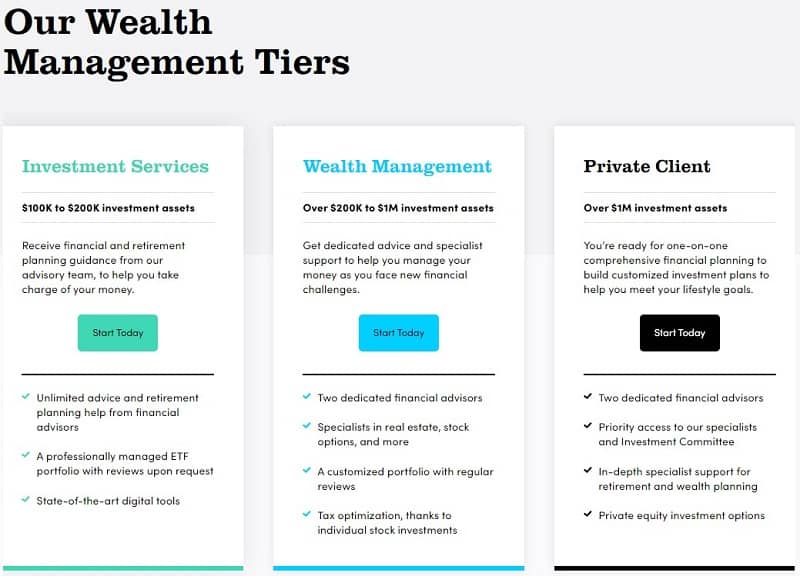

The tiers of financial plans:

- Investment Service (up to $200K in investable assets) – Access to free online tools and dashboard plus Financial Advisory Team, Tax Efficient ETF Portfolio, Dynamic Tactical Weighting, 401k Advice, Cash Flow & Spending Insights, 24/7 call access including weekends and after-hours

- Wealth Management ($200K – $1M in investable assets) – Everything in Investment Service plus Two Dedicated Financial Advisors, Customizable Individual Stocks & ETFs, Full Financial & Retirement Plan, College Savings & 529 Planning, Tax Loss Harvesting & Tax Location, Financial Decisions Support (Insurance, Home Financing, Stock Options and Compensation)

- Private Client (over $1M in investable assets) – Everything in Wealth Management plus Priority Access to CFP®, Advisors, Investment Committee & Support, Investment Portfolio Mix of ETFs, Individual Stocks & Individual Bonds (in certain situations), Family Tiered Billing, Private Banking Services, Estate, Tax & Legacy Portfolio Construction; Donor Advised Funds, Private Equity & Hedge Fund Review; Deferred Compensation Strategy, Estate Attorney & CPA Collaboration.

Empower hired advisors from other firms with a significant pedigree. My “assigned” Advisor is someone who was formerly at Wells Fargo Advisors – Private Client Group. He served as a Board Member of a not-for-profit, graduated from a prestigious university, and his entire profile is available under Advice -> Advisors.

When you talk to an advisor, you’ll discuss all the things you’d expect from any other financial advisor. You’ll start by discussing your goals, risk tolerance, future funding goals (like a house or a baby), and then build a plan that takes that all into account so you are financially prepared for the future. The management fee is straightforward, you just pay a percentage fee on the assets under management which starts at 0.89%.

👉 Learn more about Empower Personal Dashboard

Empower’s Investment Methodology

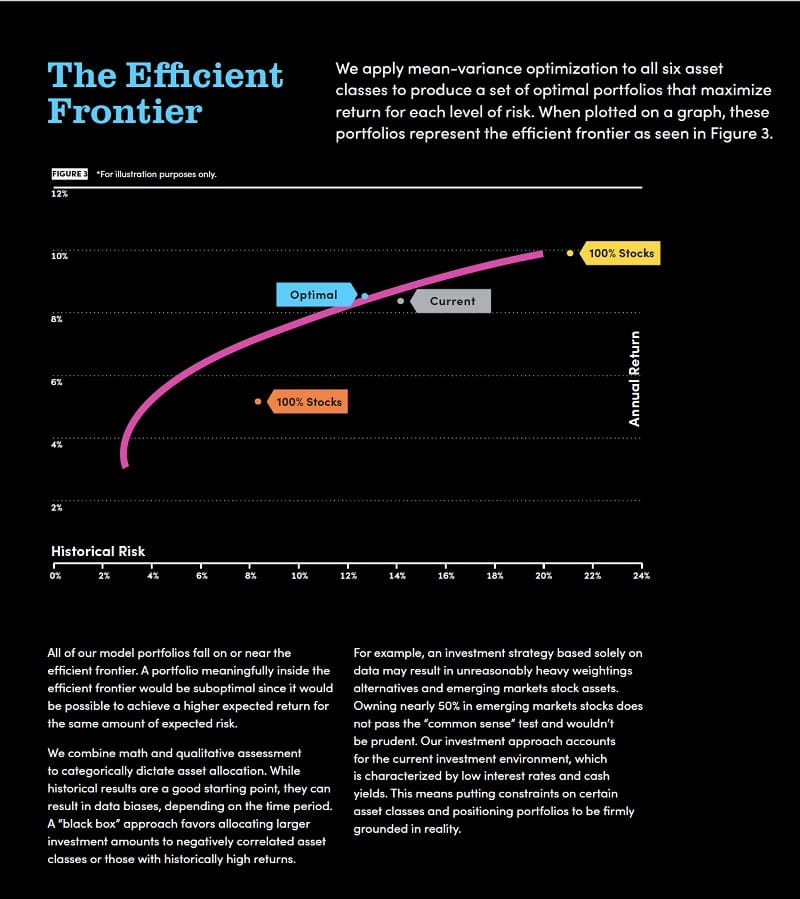

If you have Empower manage your investments, their methodology is a mixture of U.S. stocks and bonds, international stocks and bonds, alternatives and then cash. It’s based on academic research and modern portfolio theory, developed in the 1950s by Nobel Prize-winning economist Harry Markowitz. I won’t get into the details but the idea is that you try to invest in low and negatively correlated assets so that you can maximize returns while reducing risk.

There’s this idea of an efficient frontier – where you can maximize returns for that level of risk. The more risk you take, the higher the potential returns. But you want to get an asset allocation that maximizes your return for YOUR level of risk. If you don’t, you’re leaving money on the table.

Retirement Planner

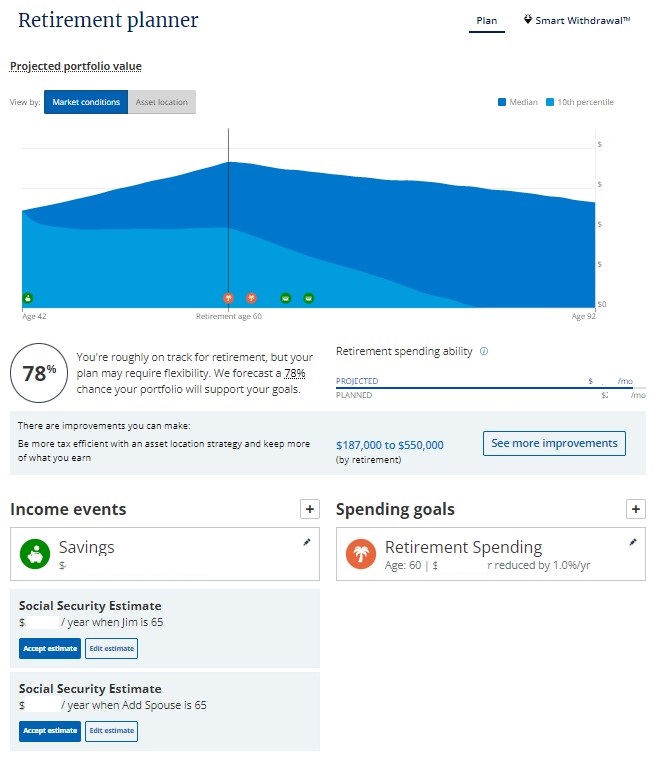

I want to dive into the Retirement Planner a little bit because it offers a benefit that few other personal finance tools do well – it’s a replacement for Quicken’s Lifetime Planner tool.

Many people use Quicken’s Lifetime Planner to help forecast retirement and beyond, so it’s nice to see some of those features replicated in Empower.

With the Retirement Planner, you set your income events – how much you’re saving today, plus how much you will receive in retirement from various sources like a pension, Social Security, spouse’s Social Security (if applicable), etc. Then you set your Spending Goals, which can be recurring like “retirement spending” or can be one time events, like paying for education. Finally, you can edit their assumptions – withdrawal tax rate, inflation rate, plus your life expectancy.

Then Empower Personal Dashboard will tell you whether you’re on track to save for this, including a detailed cash flow table that will explain how it should all play out. It’s a good way to look at the whole picture forecasted out.

Click on “How can I improve this?” and you’ll be given a series of suggestions including adjusting your asset allocation, investing more money, selling losers to offset winners, etc.

Financial Roadmap

Empower Personal Dashboard offers a tool for wealth management clients called The Financial Roadmap. It’s essentially a guide that identifies financial planning topics that they can work on with you that include everything from analyzing your insurance coverage to optimizing your pension to charitable giving. It’s a really exhaustive list of potential topics and you get to prioritize – ensuring you work on the things that matter to you. Empower will look at your data to help with the list but ultimately you decide what to focus on.

As you work on various tasks and complete them, the progress bar will advance you forward so you get a sense of where you are. There’s a complete Planning History that explains what was discussed and recommended, which can be valuable whenever you need to revisit it in the future. It helps to know what you were considering at the time of the decision, something that’s extremely hard to do many years later.

Empower Personal Cash

Empower Personal Cash is their cash management account where you can earn money on cash held with Empower. If you opt to have them manage your money, you may not always have all your cash in the market. With Empower Personal Cash, your cash balances earn 4.70% APY.

It’s FDIC insured up to $1.5 million (it’s through a number of partner banks who themselves have $250,000 of FDIC coverage) but it’s extremely unlikely you’ll ever need that level of coverage!

Additional Services

On top of the tools, the wealth management, and the financial advisor, they also offer assistance in managing three financial challenges you’re like to face – 401(k) fund allocation, insurance coverage, and college savings.

With the 401k Fund Allocation, you can send a list of the funds your 401k (or 403b or health savings accounts) offers and they will help you pick the options that fit best with your strategy.

With Insurance Coverage, they look at all of your policies and find where you might need more insurance or add policies you don’t already have. They don’t sell you insurance, they’ll just tell you what you may need.

Lastly, saving for college can be daunting but they offer support that demystifies all the different college savings options available.

👉 Learn more about Empower Personal Dashboard

Smart Withdrawal

Smart Withdrawal is only available if you are an advisory client, so it’s not free and I haven’t used it first hand.

From what I can tell from the marketing materials, the tool is meant as a calculator for when you are in retirement. It will look at your entire portfolio and tell you the optimal withdrawal order to take advantage of your portfolio’s tax situation. It will take your income sources, your retirement needs, and chart it all out for you. If you hit the age when you need to take Requirement Minimum Distributions (RMD), then the tool will take that into account as well.

Since this is only available to advisory clients, this is in addition to working with a financial advisor who you can talk through these issues with anyway.

Empower Fees

Empower Personal Dashboard is free. The website is free, the mobile app is free, and the tools are all included.

It follows the “freemium” model where the tools are completely free but you can pay if you want tailored investment advice. You only pay a fee if you use their advisors and wealth management services.

The annual fee is based on the assets they are managing:

| Assets Managed | Annual Fee |

|---|---|

| $1 Million or Less | 0.89% |

| First $3 Million | 0.79% |

| $3 – $5 Million | 0.69% |

| $5 – 10 Million | 0.59% |

| $10+ Million | 0.49% |

Empower vs. Mint: Is Empower better than Mint?

Empower Personal Dashboard gets compared with Mint.com a lot. We consider Mint the best alternative to Empower when it comes to a free budgeting app.

Mint is a very popular budgeting and money management tool that is owned by Intuit, the creators of Quicken and TurboTax (Quicken is now owned by a private equity firm). In its day, as far as personal finance management went, Mint was the gold standard for aggregation. It’s easy to use, incorporates all of your accounts, and can give you a big picture of your finances pretty quickly.

The budgeting tools are great for someone looking to track their expenses and get a better handle on where their money is going. I used it for years and watched it mature from a cool free tool that pulled your data to what it is today.

The big difference is that Mint is coming at the question of management from the income and expenses side. It’s primarily a budgeting tool with a robust suite of tools to help you get on top of your spending and servicing of debt. It’s less sophisticated in the investing department so its tools are limited in that regard.

Is Empower Personal Dashboard better than Mint? Empower Personal Dashboard is better than Mint if you are focused more on investing than budgeting. If you’re looking for a budgeting tool, Mint is better. (and if you’re looking to change your budget, You Need a Budget is even better but it has a $6.99 per month fee)

Mint was built to be a budgeting tool, so it’s investing tools aren’t even close. Empower Personal Dashboard was built as a tool to facilitate long term planning and investing, with budgeting tools added later. The big knock against Mint is that there’s very limited customer service… but it’s free (heavily ad-supported) so you can’t expect 24/7 phone support. That’s unreasonable.

If you’re at the point where you’re looking at your investments and need a portfolio management tool (AND a decent budgeting app), Empower Personal Dashboard would be a better fit. It’s also free so there’s no harm in giving it a try.

👉 Learn more about Empower Personal Dashboard

Is Empower Personal Dashboard Safe?

As you’d expect, security is extremely important and should be with any software that even has a peek into your money. Empower Personal Dashboard uses AES-256 bank-level encryption and has two-factor authentication.

Empower Personal Dashboard will require you to register each device you use and will periodically request you to re-register them in a bid to keep you as secure as possible.

Internal controls are another strong suit – no employee has access to your information and it’s your account information is encrypted and stored at Yodlee. Yodlee has powered a lot of other company’s data for this purpose (they were the ones that supported Mint’s data for a long time) and they have strong encryption as well.

We asked Dr. James Curtis, professor of IT and Cybersecurity at Webster University, for his thoughts on security and the cloud:

The cloud is generally no less or more secure than a standard organization’s own network system. All computers, storage platforms, or transmission systems have the same vulnerabilities, with people being the single largest vulnerability of all risk elements. Utilizing standard security procedures is a best practice for cloud providers like Amazon, and they are quite adept at ensuring they comply with these best practices and standards such as the NIST standards for cybersecurity.

I do believe there is one area of concern that is more of a perception issue than anything else – the fact that the owner of the data doesn’t have direct control over the data because they are relying on a service-oriented model by contracting with a cloud service provider. So, essentially the cloud provider is asking the data owner to ‘trust’ them to keep their data secure.

I think this is not an issue with a reputable cloud service provider, but it is a risk factor that organizations should consider when deciding to outsource their data to a cloud provider, especially if they deem their data so sensitive that they need more stringent controls over it than is standard.

As for trusting companies like Mint and Empower Personal Dashboard, he shares:

In some ways this is similar to the cloud security risk management issue. While I would argue reputable companies like Intuit that own Mint are just as reliable as the cloud service providers like Amazon, and that they comply with the same security standards and best practices, there is a different type of risk associated with these applications because they are software-based applications requiring the highest levels of security to protect the data. Many of the issues with cloud services are related to transmission and storage of the data, while financial applications such as Mint and Personal Capital are more susceptible to risks by hackers who target single users or organizations.

About 80% of security risks are associated with the software of a system vice the hardware, transmission media, etc. As long as the user follows standard security protocols such as password protection, firewall, and virus monitoring and management, and other related cybersecurity defenses, these financial applications are as safe as any other mainstream applications

No system is 100% safe but this one is pretty close. We take a much deeper dive into safety and data security at Empower Personal Dashboard and feel confident in their systems and processes.

What Needs Work?

In the first edition of this review, I had issues connecting with TradeKing because TradeKing had a different authentication system.

My original solution was to put all of my holdings in a portfolio and Empower Personal Dashboard tracked them separately. When Ally Bank acquired TradeKing, turning it into Ally Invest, it was now automatically tracked.

You can’t import historical data, so you only get about a month of history based on when you signed up. There’s no way to import data from Quicken or upload from historical downloads from financial institutions. Your history starts from when you sign up (about a month before that, based on how your financial institutions report transaction data). It’s a known limitation and there isn’t a plan to add historical data support in the future.

The budgeting tools need more work but it’s relatively new so I expect growing pains. It’ll improve but it still gives me the knowledge I need, monthly income and expense values, even if the categorization needs more hands-on help.

Final Word

Right now, Empower Personal Dashboard is my tool of choice when it comes to managing money and investments. At this stage in my life, investments are becoming a more significant part of our finances and so having visibility into that area is crucial.

I recently started using personal capital. So far so good. I like you enjoy the benefit of having all my accounts rolled up into one place. Its a time saver.

That was the #1 benefit for me, the rollup since I couldn’t pull TradeKing data into Vanguard.

I’m not too thrilled with Personal Capital. I’ve been using it for around a year. There’s a problem of some kind every couple months. Sometimes, there are issues connecting to accounts. Sometimes, accounts are listed multiple times. I’ve had an issue where it was taking the balance of one account at a source and listing it as the balance of other accounts at the same source. As of right now, it’s been more than 3 months since I’ve been able to connect to the brokerage (one of the largest in the US) where the majority of my assets reside. It’s… Read more »

Right now TradeKing isn’t tracking directly, I had to replicate my portfolio and thus it won’t update itself. It’s been like that for a couple months, though I’m not sure what the hold up is.

I’ve been using Personal Capital as well but struggle with the authentication process. My bank has a number off hoops to jump through to sign in using an outside system so it can be cumber some. Because they are a growing company, customer service isn’t instant but doesn’t take two weeks either. I want to keep using it in hopes of gaining better picture of my retirement plan.

I have yet to contact customer service so I don’t know, but so far my banks have authenticated without issue. I realize I may be lucky though.

Unfortunately the problem you have with your TradeKing accoount is an inevitable side effect of sites like this and Mint. Any time a bank or brokerage website updates its API, Personal Capital has to update their code to properly interact with it. It seems like it would be a huge ongoing maintenance project on their part. I can’t say I envy the developers over there, haha. Luckily for me, I just love monitoring my accounts by hand. I really enjoy checking in on all my accounts to see how well I’m doing, and what needs improvement. It makes me feel… Read more »

I did enjoy a more hands on approach, especially when I review my accounts every month, but I found the logging in process understandably cumbersome. Plus, rolling up the data is a better way of viewing my accounts anyway.

Back in the day, everyone just used Yodlee to do the data collection. They had links to banks, or scraped pages after logging in, and so you had just one point of failure/maintenance. I don’t know if PC took that in-house but I doubt it. Give it shot and let me know what you think.

I’ve been using Personal Capital for a while now. For the most part, it work well and is very convenient, but, unfortunately, it doesn’t connect very well with smaller financial institutions like Robinhood.com or small mortgage providers.

I think the online capabilities of some of the smaller mortgage providers is probably lacking so there’s nothing to hook into. As for Robinhood, they don’t even have a web interface right? It’s 100% via the app?

I think all aggregators would have problems with those since there are no hooks?

Yes, you are correct on both counts.

Robinhood is only available via their app.

Also, Personal Capital allows their users to manually enter the dollar amounts of the smaller financial institution accounts into PC. If it’s one or two, it shouldn’t be too bad.

I have it monitor my TradeKing account by holdings, rather than direct link. So there are workarounds and for me it’s just one account.

You are actually incorrect Robinhood has a web interface at Robinhood.com

Ha, somehow the dates on my comments disappeared but that was an old one – there is a web interface now.

I haven’t used Personal Capital but I have heard lots of good things about it, and by the looks of it, I think it has to potential to manage your personal finances pretty well, even if you don’t use your account for anything other than simply tracking your net worth.

Give it a shot and let me know how it goes!

How does this site differ from a site like draftapp? Trying to decide which one to use.

I haven’t used draftapp first-hand but as I understand it the tool compares your investments with other people in various peer groups with an eye towards lowering your expenses and establishing a solid asset allocation. Personal Capital is an aggregator of your finances, which includes accounts outside of your investments (like bank, credit cards, etc.). The primary focus is also investments but it has the other parts of your money system tied in. DRAFT is laser focused on investments, PC is broader and has a bit of the expense management portion built in too.

Like Sara, I’m also trying to decide, have you had any experience with Mint and if so, how does this compare to PC ?

I used Mint and it was good for budgeting and tracking expenses, it was (and from what I can tell, still is) bad with investing and portfolios. It was never designed to be for investments though, so you can’t fault it for that. I think Mint’s budgeting features are better than Personal Capital but Personal Capital’s investment tools are far superior. If you think about the two and their history, Mint started as a budgeting tool to compete with Quicken. Personal Capital started as an investment tool to compete with robo-advisors. So their respective strengths are still in their original… Read more »

This is a general call out to find out if anybody has used their financial advice service. I have a work 403b from a job I left and am looking to convert it to a traditional IRA (and then maybe concert to a Roth IRA if I can get my head wrapped around how that works). My options are to get a vanguard account (no current account now) put it in betterment where I have some money, or now that I signed up for this personal capital account, wonder if I should use them. Just curious if anyone has any… Read more »

I tried Personal Capital and loved it until I realized someone else might have access to all my financial info. It’s not clear how much is shared with these investors in the shadows. Am I the only one concerned about this?

This is something all of these companies have to deal with and they have more to gain from keeping your personal information private. Security is always a concern when you put all this information out there, that’s for sure, and it’s a completely valid one. I’m comfortable with it though.

One thing I’ve discovered Personal Capital does is log into your account more than once. I logged into my bank this morning at 11:59 and the bank’s website said the last time I logged in was 11:36 this morning. That was a little disconcerting since it wasn’t me. I contacted the bank and they were able to figure out by IP address that it came from Yodlee which is what Personal Capital uses for authentication. I know it’s read only and they can’t do anything with it but I’m not sure why they do it more than once and perhaps… Read more »

I’m not surprised but I wouldn’t have expected it, I’d love to hear what they say, can you keep us updated?

They pull data every 24 hours or when you login Personal Capital. This keeps the data on PC recent, so it is fresh when you login.

This looked exciting to me since Quicken helped me get control of my finances years ago. But one thing that concerned me was how they actually linked the accounts. For some links, they want you to provide the actual username and password for accessing the account. I wasn’t very comfortable with that. But I did find that you could do manual investments where you just tell it your stock holdings and it will pull stock prices and update your net worth. It might mean extra work for me whenever I buy/sell something, but it gives me a little bit more… Read more »

If you’re uncomfortable logging in (which is how all the tools do it), manual investments is the best alternative and they can update it based on that.