Synchrony Bank

Strengths

- Competitive interest rates

- No minimum balance

- No ATM fees in-network, $5 monthly rebate out-of-network

Weaknesses

- Online bank only, no branches

If you've never heard of Synchrony Bank, but seen it advertised everywhere online, you wouldn't be alone.

In fact, if you looked prior to 2014, you wouldn't have seen Synchrony Bank anywhere. Then, in what appears to be an instant, it was everywhere.

That's because Synchrony Bank was founded in 2003 but operated as a subsidiary of GE Capital. It's now a retail bank but they don't discuss their history much. It would IPO in 2014 on the NYSE with the ticker SYF to the tune of $2.88 billion. It didn't appear out of nowhere unless you consider an IPO “out of nowhere.”

(does this story sound familiar? Ally Bank was once General Motors Acceptance Corporation, GM's financial services arm, and these stories rhyme)

So who is Synchrony Bank?

About Synchrony Financial

They're a financial services company based out of Stamford, CT and they offer everything you'd expect from a bank – deposit, credit, financing, and lending. In layman's terms, that's checking and savings accounts, credit cards, mortgage, car loans, and the like. They also provide private label credit cards (they're one of the biggest), so they are the backbone behind some popular retailer credit cards like Amazon, Lowes, Walmart, and Gap.

Synchrony Financial is the parent company, Synchrony Bank is the institution that provides those products. They're FDIC insured #27314 and they're headquartered in Utah.

Synchrony Financial (SYF) had revenues of $13.530 billion in 2016 and is a component of the S&P500 index.

Synchrony Bank has just one physical branch in Bridgewater, New Jersey – 200 Crossing Blvd, Suite 101, Bridgewater, NJ 08807. Branch is open Monday – Friday from 8am to 3pm EST.

You can contact Synchrony Bank customer service by calling 1-866-226-5638 (Monday – Friday 8am-10pm EST, Saturday 8am-5pm EST, Closed Sunday). The Synchrony Bank login is here.

Synchrony Bank's routing number is 021213591.

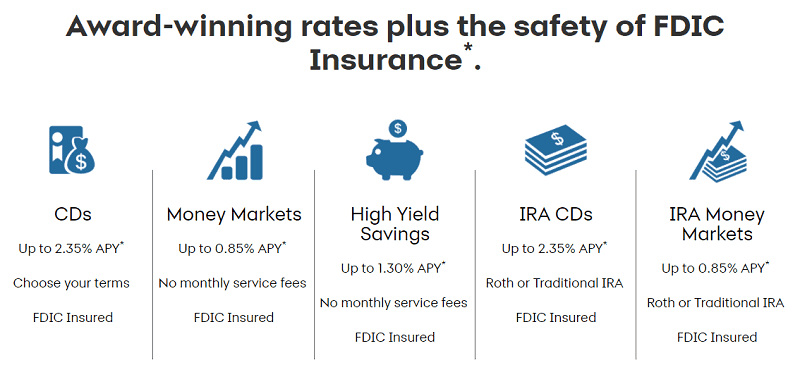

Synchrony Bank Deposit Products

Synchrony Bank offers the full menu of deposit products – money market (similar to checking), savings, high yield savings, certificates of deposit, and even IRA accounts.

All rates cited are as of 4/3/2023:

- High-Yield Savings: No monthly service fees, 4.75% APY, no minimum balance.

- Certificates of Deposit: Maturity periods of 3-months to 60-months, $2,000 minimum deposit and the 12-month CD yields 4.50% APY

- Money Markets: No monthly service fee, mobile check deposit, no minimum balance, up to 2.25% APY

- IRA: You can open a regular IRA account or an IRA CD account.

Synchrony Bank Credit Card

Synchrony Bank's credit card, called the Synchrony HOME Credit Card, is a no annual fee credit card that is a card for home purchases that offers promotional financing of 12 months to 60 months at participating retailers. They are mostly home furnishing or home improvement stores. It also offers 2% cash back on purchases under $299, paid as a statement credit.

Synchrony Bank also issues several white-label credit cards, meaning they're run by Synchrony Bank but they are branded with others names. One popular Synchrony Bank powered credit card is Amazon.com's Amazon Prime Store Card – which gives you a $10 Amazon.com gift card upon approval plus 5% cashback at Amazon.com with no caps. No annual fee, special financing on orders $149 or more, and all the typical protections of credit cards, like $0 liability.

They also power other retail cards like American Eagle Outfitters, Athleta, Chevron, Old Navy, PayPal & eBay, Sam's Club, Toys “R” Us, Walmart and more. If you have one of those cards, you may have seen SYNCB appear on your credit report. I had SYNCB/PPC and was surprised to see it because I didn't know it stood for Synchrony Bank / PayPal Credit! It's normal though, just looks weird.

Synchrony Bank Fees & Penalties

Like many online banks, there are no minimum balances for their savings or money market accounts. There is also no monthly service fees.

What is rare is that they will not charge you a fee if you exceed six withdrawals/transfers in a statement cycle. Many banks will charge this because you aren't supposed to (according to the Federal Reserve) treat a savings account like a checking account, but Synchrony won't. They do, like other banks, reserve the right to close your account if it happens too much.

With their CDs, there is an early termination fee if you make a withdrawal from your Cd before the maturity date:

- Term 12 months or less: 90 days of simple interest at the current rate

- Terms of more than 12 months but less than 48 months: 180 days of simple interest at the current rate

- Terms of 48 months or more: 365 days of simple interest at the current rate

These interest penalties are fairly standard – it's the exact same as what Bank of America and any major bank would charge.

The gold standard of CD rate penalties is Ally Bank:

- Term 24 months or less: 60 days of simple interest at the current rate

- Terms of more than 24 months but less than 36 months: 90 days of simple interest at the current rate

- Terms of more than 36 months but less than 48 months: 120 days of simple interest at the current rate

- Terms of 48 months or more: 150 days of simple interest at the current rate

It's almost unfair to compare the penalties with Ally Bank because they are far and away the lowest for early withdrawal.

Loyalty Perks

Synchrony Bank also offers “Loyalty Perks” that reward you for saving.

Whereas most institutions, like credit cards, will reward you for spending – Synchrony rewards you for saving.

The Perks Tiers are based on your balance and time with Synchrony:

- Basic: Balance under $10,000 AND less than 1 year

- Silver: Balance of $10,000 – $49,999.99 AND 1+ years

- Gold: Balance of $50,000 – $99,999.99 AND 2+ years

- Platinum: Balance of $100,000 – $249,999.99 OR 3+ years

- Diamond: Balance of $250,000+ OR 5+ years

Sadly, Synchrony Bank does not have any new account bonuses right now.

Pros and Cons

The main pros are similar with other online banks – you get low/no fees, a wide ATM network due to partnerships, debit cards, much higher interest rates, and the smartphone apps are more powerful. They offer free checks for the money market account and there is $5 in ATM reimbursements. The Loyalty Perks are a nice add-on we don't see elsewhere

The cons are similar too – there no branches you can visit and everything happens via the app (or perhaps mail) or online. You have to be comfortable with working with a bank entirely online if you want to go with Synchrony Bank. I personally have no issue but if you're not comfortable, Synchrony Bank would not be a good option for you.

Conclusion

Synchrony Bank is fine but doesn't really excite me in any way.

I don't ever suggest rate chasing, switching banks for the best rates, but if you're #1 bank is an old brick and mortar bank with abysmal interest rates… it's worth a look at this high-yield savings account.

Hey Jim! I’m a huge believer in online banks; switched about 5 years ago and never looked back. The only reason I can think of to have a brick-and-mortar bank is if you need to frequently do large cash deposits and withdrawals (and in that case I would probably use a credit union).

I still see a lot of people, though, that like to personally know the people that work at a bank, and are very reluctant to switch to online banking because of that. But I’d say that’s costing them money.

Cash transactions (and how rare are those!) are one of the few reasons to have a brick and mortar bank account… maybe also medallion guarantees (even rarer!).

We have the Amazon store card which is by Synchrony. I didnt know they offered a high interest rate at 1.30% (with no minimums.) My husband went with Discover at 1.10% because it was the easiest (no upkeep, no minimum etc.) but I think we should have shopped around some more.

Haha are these real replys above me? Synchony bank is a joke, i currently have three different credit accounts and all are over 25%. I had to take out a loan from my current good bank SECU to pay the one care credit account I have through them. Making more than minimum payments don’t help. Will never recommend them to anyone.

You’re talking about credit, this was more of a review of their deposit products. Your interest rate will be a function of your credit score as well as other debt related factors. If you feel it’s too high, I’d recommend trying to find a balance transfer to a lower rate card.

Syn-crappy Bank is a joke. It price gouges the public on basic credit cards for staters and does not pay that much on CD’s or savings. So why would anyone recommend them unless they work for them? I just cancelled 2 credit cards with them for TJ Maxx, & Amazon because they price gouged me by tacking on an EXTRA $27.00 late fee for one month. Now I only have 2 credit cards, and only because they offer (I thought), good perks, but this past month Syn-Crap took liberties and charged me an extra $54.00 in total for me not… Read more »

I always get the bill in the mail for my loan 4 days before the due date. I send it out the next day – 3 days before the due date. I figure it takes the Post Office 2 days to deliver it (maybe 3). Synchrony Bank apparently takes a day or two to get it through their “system”. So every month my payment is marked as “Late”. They “can’t mail [my] bill out sooner”, and suggest automatic deduction. You can’t pay online (it is the ONLY loan I have that I can’t pay online!). You can’t even set up… Read more »

That’s incredible… no online billpay???

I have used Synchrony to finance a project. NEVER AGAIN! The interest rate jumped up to 29.99 % after the promo period, which is understandable – I agreed to that. I got hit with deferred interest – I slipped. My fault. However, after over 3 years of faithfully paying my bill, they still refuse to lower my rate. I repeat, NEVER AGAIN. I will pay these leeches off, and if I ever have another customer that wants to finance with them, I’ll walk away.

I agree that your post has to do with banking and not credit. However, the company name Synchrony is much more identified with their credit cards. And with that, they are an awful company to work with. I have had credit card companies that have switched and now I shudder when I hear their name. When applying for credit and hear their name, I cancel my request and seek another lender. There are so many customer service and credit companies that deal with all types of consumers, it’s worth shopping around. We deserve better.

My experience with Synchrony bank is hassle free.I recently got a credit card from Walmart which is financed by Synchrony bank and on the very first statement I observed an error.I pointed this out to customer service an the error was corrected without delay. Another positive experience was with my third statement where a supplier/merchant attempted to bill me monthly without my permission.Again ,a call to customer service corrected this issue. Please note that my card payments are done online since I set up an account to transfer my credit payments.

Our 19-year-old daughter had her Chevron card declined last week, because she made the mistake of using her card near home, while we were traveling out of state. Apparently, that constitutes ‘suspicious activity’ to Synchrony Bank. This is very troubling, because a Chevron card is not like most others, in that with most other cards, declining the card won’t leave you stranded, possibly in the middle of nowhere. Declining a card like Chevron can have some very real personal safety consequences. We have never had issues with our Chevron cards since 1980, but after our experience dealing with the idiots… Read more »

Isn’t that the fault of Chevron?

I don’t think it’s a problem with Chevron at all; in fact your flip reply indicates that you are receiving a kick-backs from Synchrony. To be more specific, before allowing a Chevron branded Synchrony C.C, an inquiry/permission request in made to the issuing financial institution. Synchrony, without bothering to check, decided that the daughter, who has a family type card, was not in the area of the primary account owners, could be a card thief, and declined her purchase which in fact could have stranded her in a rest stop somewhere (or worse). As Synchrony, in the world of cell… Read more »

They also manage BP cards and I have had similar issues. I have had a BP card since 1984 when it was Amoco. I closed it today because the idiots at Synchrony cannot figure out when it’s me and when it’s not. Their loss. Unbelievable!

I’ve been a Synchrony customer since GE Capital. I own both credit and deposit accounts , no issues , no worries.

Credit cards are deeply affected by Federal Reserve actions and of late it’s not a borrowers market however I pay off at the end of each month, still no worries.

Synchrony is easy to deal with and that’s it plain and simple. Rates are great and services are available online 24/7 so what’s not to like?

I can highly recommend Synchrony Bank.

I got a syncrony card through amazon. I opted for online billing. The first time I logged in they locked my account for suspicious activity and told me to call their office number. I called the office and they said a pin would arrive in a few days to unlock my account. The pin arrived 3 weeks later and when I called it in I was told it was an invalid pin and my account would remain locked. Unable to pay online (account locked) I called syncrony and asked for a paper bill, no bill came, but I got a… Read more »

Okay….Are you aware Sr. that Synchrony Bank offers their customers 100% fraud protection on the cards they service? They have thunders if not thousands of frodulent charges they have to staff people to investigate and charges they have to eat and they do eat them. I think with that kind of protection they give you a short hold up to place a call to tSynchrony in order to verify the validity of the suspicious charge isn’t as big a deal than itt would be if you were left without that fraud protection and held liable for the fraudulent charges. Those… Read more »

Terrible customer service, complete with flippant attitudes due to highly restrictive policies and antiquated methods (i.e requiring you to fax or mail documents), rude managers, long transfer times into and out of the accounts. Save yourself the frustration and never do business with this bank; it’s not worth the man hours it will take you to get anything resolved should you ever have an issue and in the meantime, they will simply deny you access your money for weeks or longer.