In early November, on his radio show, Dave Ramsey offered up some advice that was flat out wrong.

A caller was asking about retiring early and safe withdrawal rates. A short clip was posted on Twitter/X by Marvin Bontrager in which Ramsey seemed to get upset and annoyed at one of his own team members, George Kamel, for offering up 3-5% as a safe withdrawal rate. (he called people stupid and morons and became visibly annoyed and almost angry during the clip)

The crux of his argument is that 4% safe withdrawal rates are too low. He continued to say that if you can get 12% from the stock market you can safely take out 8%. Then he started calling people nerds and living their mom’s basement with calculators and saying 4% is stealing people’s hope.

Then he, essentially, finishes by saying that a million dollar nest egg should create an $80,000 annual income perpetually.

Table of Contents

Beware When Experts Get Emotional

Do you make your best decisions when you get emotional? Happy or sad or angry or whatever – you probably would agree that the best decisions are made when you’re level-headed and not fired up.

You don’t want your financial advisor to get emotional. You don’t want them to get worked up. You don’t want them to talk about members of their team the way Ramsey did with his. They say that an early and extremely reliable indicator of divorce is contempt. It’s not good for any relationship.

You want someone who is calm, collected, and is (if we are to be perfectly honest) a calculator-carrying super nerd.

Also, be careful whenever someone replaces facts with emotion. It’s hard to have a calm discussion, especially on air, with someone who is getting upset. It’s doubly hard when that person is your boss, signs your paychecks, and has their name on the wall right behind you.

8% SWR on $1mm = 67.5% Failure

Dave Ramsey says that a $1 million nest egg should provide you with an $80,000 annual income forever.

FICalc is an easy to use calculator (you don’t need to be a super nerd or live in a basement) that will run simulations and give you a success rate given your input parameters. We set the portfolio (its the default) to 80% stocks, 15% bonds, and 5% cash with a withdrawal rate of $80,000 a year.

In 123 retirement simulations, only 40 were able to sustain withdrawals for 30 years.

When you drop the withdrawal rate to $40,000 a year, the success rate jumps to 96.7%.

Go ahead and play with it yourself but the answer is clear – if you follow Dave Ramsey’s advice on withdrawing your nest egg, there is a 67.5% chance you will become penniless.

Facts: A 12% Return is Not Realistic

The reason why 8% withdrawal rate doesn’t work is because a 12% return is not realistic. It’s simple math.

Dave Ramsey says he makes 12% easily through a decade. You can even see Rachel Cruze, his co-host in this clip, try to walk things back a little by discussing what you’d do with a 10% rate of return.

Even if you accept that you can make an average of 12% over a decade, the true killer is what’s known as sequence of returns risk.

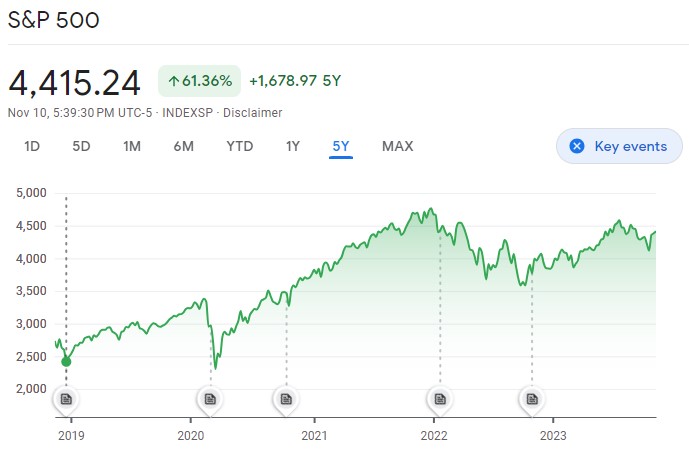

Check out the last five years of the S&P 500 index:

It’s lumpy. It’s really lumpy.

If you didn’t touch your money (or better yet, kept contributing), you’d feel great about making 61% over five years. It’s about 10% a year but it’s not 10% every year.

You can see those time periods in which the market return nothing. From 2019 to early 2020, when the pandemic hit, we see a return of zero (or less). From early 2021 to late 2023, you can see how the market went up above 4,500 in late 2021 only to fall back down below 4,000 in 2022.

But when you’re withdrawing on a regular basis, you’re pulling money out at times when you need it for expenses. The sequence of returns risk is the risk that you’re selling when the market is lower. If you’re retired, you can’t pick and choose and so you’re subject to this risk and it’s what sinks retirement portfolios… especially those with too high of a withdrawal rate.

Dave Ramsey is Good At Debt

Dave Ramsey has helped a lot of people get out of debt. I was never in high-interest debt and so I never listened to his work or read his books. I’m familiar with his debt snowball and other debt payoff strategies.

What this has highlighted is that when someone is good at one aspect of something (in this case, personal finance), it doesn’t mean he’s good at all aspects of the subject.

He has helped a lot of people get out of debt. It makes him a great expert to listen to on the subject of debt.

When we get into investing, that may not be the case. With paying off debt, you want that emotion because the steps are easy and without nuance. Sometimes you need a little scolding so you don’t spend when you shouldn’t.

With investing, you want as little emotion as possible and as many calculators as possible.

In this case, Ramsey’s strength turns out to be a weakness.

Other Voices Weigh In

Since I’ve been blogging for quite some time, I know a lot of other personal finance folks and nearly everyone has weighed in on this… and the response has been unanimous.

First, the super nerds united. David Blanchett, Michael Finke and Wade Pfau co-wrote a piece for ThinkAdvisor titled Supernerds Unite Against Dave Ramsey’s 8% Safe Withdrawal Rate Guidance. It’s a bit meaty with some math but the headline is the same – “you would have needed $3 million to maintain an 8% rule for just 22 years.”

Next, I want to show you this post from 2019 from ESIMoney.com because it actually cites a much earlier time when Dave Ramsey has claimed 12% market returns. It cites a Seeking Alpha article that states – “Started in 1934, the ICA has averaged a 12.13% annual return since inception. When Dave says there is a mutual fund that has averaged 12% since 1934, he is telling the truth. To validate his claim, the Pioneer Fund (MUTF:PIODX) has averaged 11.88% since 1928, so there is evidence to prove Dave’s thesis.”

While Dave’s 12% number has a little support, the numbers matter because 12% and 10% are wildly different. Read ESI Money’s whole article and you’ll see why 12% isn’t crazy but it’s a bit misleading.

The Frugal Expat recommended that you check out Rick Ferri instead. I agree.

Another point of reference, I want to send you over to Karsten at Early Retirement Now. If you wanted to meet the head super nerd with the calculator (said with much love, admiration and respect!), Karsten is your person. His post How Crazy is Dave Ramsey’s 8% Withdrawal Rate Recommendation? is required reading.

Finally, my friend Cody shared this on Instagram:

Thanks for Dave Ramsey article.

Yes, he has helped many get out of debt…..which he once was in.

Most of need more knowledge of RMD’s and other things.

Keep up the good work.

Years ago, I helped facilitate Dave Ramsey’s Finacial Peace University program at our church. He was a condescending prick then and he still is. He made comments like “show me the person who claims to have gotten a free flight by using a credit card so I can call them a liar to their face. Granted, the vast majority of the participants in the course were there to get out of heavy debt. I understand that using credit cards isn’t a good idea if you struggle with paying them in full each month. However, Ramsey speaks of credit and debt… Read more »

He does get oddly emotional about certain things, which is off putting, but I guess some people like that? Tough love?

Sounds like you had some fun and if that makes you a liar or idiot in his eyes, so be it!

Maybe some of his followers need that type of language to follow through? I never felt a need to talk to people like that but I also grew up differently. You can be tough but being condescending is just cruel.

Good work on debunking Dave Ramsey. I agree with him on debt but we with mortgages know not all debt is bad. Years ago Peter Lynch a very good mutual fund said you can get 10% a year and take out 10%.