‘Tis the season to get scammed! With billions of dollars swirling around the internet, it's no surprise that credit card fraud would be on the rise.

One of the more unorthodox things I do is get credit card transaction notifications via email. On any amount greater than $0.00.

That's right, I get every last transaction.

Why do I do this? It started on a whim. I was thinking about how to build a do it yourself identify theft system and found this feature in my Chase Southwest card. You can set it to notify you for any transaction over $X – where you set the X.

So I set it at zero!

I've heard a lot of scam stories. A lot of them are people getting ripped off for small amounts, like $5 and $10 over a long period of time. It works because they don't notice.

Sometimes, scammers like to do little test transactions to see if the card is real. If the little charge goes through, then they go after the big stuff or they sell the information to someone else.

I figured that if I set it up like this, I'll know about fraudulent charges immediately and I can dispute the charges with the credit card company.

In a little revisionist history, I started saying I like to know when my credit card is being used… because after a while, I kind of did. The notifications happen near instantly too. By instantly, I mean I sometimes I get the notification before the server has come back to the table with my card!

That's how fast the notification arrives.

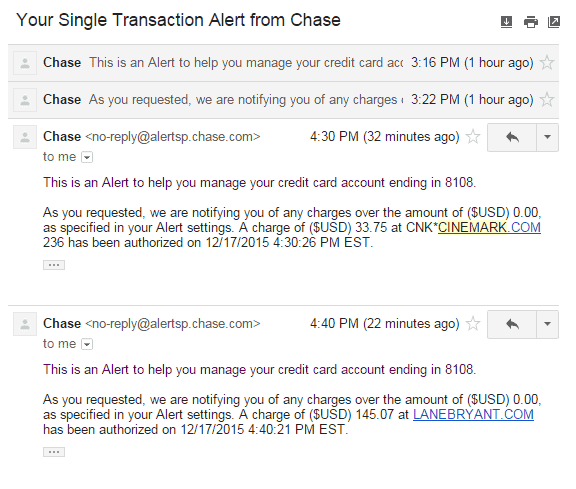

So imagine my surprise when I get these two emails about charges I didn't know about!

Great! The system it's working!

It was the holidays, my wife and I share a credit card to maximize our rewards, and so it's possible she purchased from these vendors as gifts. Except they're not because my lovely wife is sitting right next to me and told me she never made these purchases. Fraud!

I call up Chase, get transferred to their fraud department, and learn that these were made online from Pennsylvania. The call took all of 9 minutes because I didn't have to sift through a list of transactions trying to guess what is legitimate. I knew exactly what I was disputing.

Added bonus? I'll be getting a card tomorrow via express mail because it's our daily use card (that's a term you have to use if you want next day delivery of a new card, otherwise it goes regular mail).

If your card offers it, you should sign up for transaction notifications.

It sounds extreme until you realize you probably don't use your card as much as you think and it has the added bonus of reminding you of subscriptions you might not use all that often.

Win-win.

How to Setup Transaction Notifications

In general, each credit card company sets it up in a similar way – through their alerts system at the account level. You typically have to log in, go to your profile, and find the area that controls alerts. Once there, you can give them permission to email you, text, or even Apple notify you of transactions.

Below, I've explained how to do it for American Express, Chase, and Citi because we have their cards.

American Express

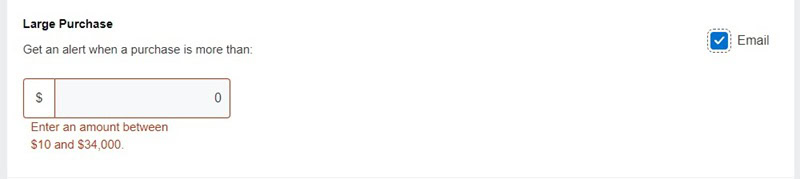

American Express will let you get a notification via email on a transaction but only if the amount is greater than $10. This means that smaller transactions won't trigger it and there's no way to set the amount lower.

To do this, go to Account Services -> Alerts and Communications Preferences -> Account Alerts. Then, scroll all the way down to the Large Purchase alert.

Chase

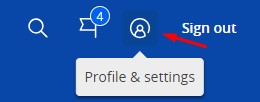

For Chase cards, it's all managed through Profile & settings. Log into your account and click on the Profile & settings link at the top right, it's the circle with a person in it:

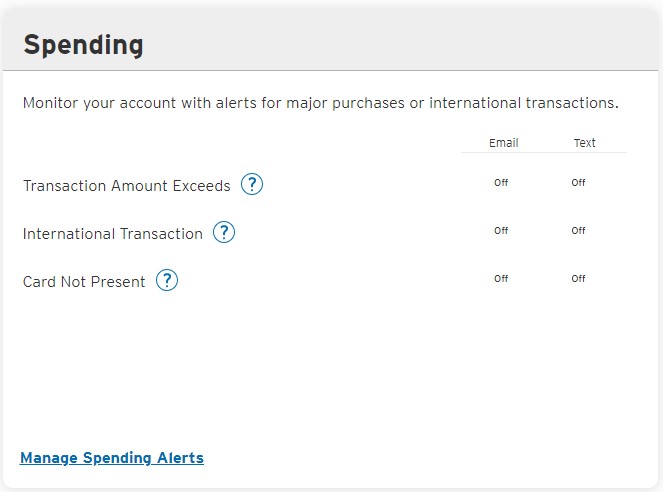

Then, in the left menu, you want to go to Alerts and “Choose alerts.” Transaction notifications is located under Protection and security:

You can set it to send you an email, Apple notification, or text whenever you get a charge (I set it to $0 so I get all transactions). You will have to do this for each card separately.

You can get notification for:

- More than $__________ (USD) is charged to my card for a single transaction

- An international charge has been posted to this account

- An online, phone or mail charge is authorized on my credit card

- A gas station charge is authorized on my credit card

- A credit is pending on my card account

Citi

For Citi, click on your Profile in the upper right and go to Account Alerts.

Then, scroll down until you see the Spending box on the left and you can manage those alerts:

Click through and you can set these values. You can set the transaction alert to $0.00 so that you get all transactions.

Michael (The Honeymoon Guy) says

Love this tip! I use transaction alerts also but never set the threshold to zero. Will try it out.

I thought I was going to get a deluge, then I realized that would only happen if I make a ton of transactions. 🙂

Brian @DebtDiscipline says

I have the Southwest Visa too, and have alert set up, need to double check my alert threshold. Great tip!

Thanks Brian — you can set it to $0, I was surprised. All the credit cards I have will let you get alerts.

Bill at FamZoo says

Love this! Just set it up for my Wells Fargo VISA card. They require a min of $1.00 or more, but that’s still a winner.

That’s awesome! $1 is a good enough minimum, I can’t remember the last time I got a charge under a dollar (not counting iTunes).

Fred says

Th8is is a really cool idea. I’m going to have to lower my threshold from $500 to zero.

Thanks Fred! I thought about what my threshold would be and thought why not try $0… then these two hit and I realize a $100 limit would catch one and not the other (and I probably wouldn’t have noticed Cinemark if I reviewed my transactions, since we occasionally go to movies). $0 isn’t that bad normally, but it does get tricky during the holidays. 🙂

Leigh says

I use this for my checking account because I’m more worried about that one than a credit card. Credit card fraud is a bit less urgent. I think I set mine to > $0.01 since I didn’t think I could do > $0.00!

I think $0.01 and $0.00 are functionally equivalent. 🙂

Mike says

A long story for you:

My wife has a slight spending problem so I had set up these alerts for anything over $100 to try to combat her spending habits. I was at work around 10am and got an alert that we spent $711.42 at a Walmart store near our house. I quickly called my wife and she didn’t answer. It was possible she had to buy something for work, but unlikely. I called another 10+ times, no answer. Then I used FindMyiPhone and was able to see she was at work still. I quickly called the police where the Walmart store was located and they were useless. All they told me to do was call my credit card company to cancel my card and a detective would call me back within 72 hours.

I was on a mission. I drove to Walmart and ran to electronics to see if anyone bought a TV or something $700+ in the last 18 minutes. Nope. Nothing.

Then I remembered that Walmart will reprint a lost receipt if you know the date of purchase and the credit card it was bought with. So I went to customer service and they said they had found two receipts and she would reprint them for me. Two receipts? I only got an alert for one! The second receipt was under $100 so no alert. I quickly changed my alert limits $1.00.

I wanted to know if this thief went through a fast food drive thru for lunch. By this time, my wife had called me back and I asked her where her wallet was to which she replied, “in my purse behind my desk.” I asked her to get her wallet out and look for her Chase card and she screamed and said her wallet was missing (side note: she wasn’t worried that her identity had potentially been stolen and our financial future had been compromised, she was worried that someone made off with her $170 wallet I got her as a Christmas gift and a $20 store credit to Victoria’s Secret. Not a single shred of concern for the book of blank checks, her drivers license, countless credit cards (she isn’t allowed to have a debit card – that is too dangerous), insurance cards, etc.).

She had gotten a drink at Dunkin on her way to work so she knew she had her wallet in the last couple hours. A quick search of her car turned up no wallet. By this time, her coworkers had inquired of her screaming and commotion and one of her coworkers told her she had to tell a patient she wasn’t allowed to wait in her office while my wife wasn’t in there (she was in a meeting which is why she didn’t pick up my 200 phone calls). My wife works at a sort of pediatrician’s office for lower income families.

So after I had heard this, I had guessed the unattended visitor made off with her wallet. So when the Walmart person came back with the receipts, the $711.42 was for jewelry and the the $70.09 receipt was for diapers and formula. Mind you the time stamps showed she bought the $700 ring before she bought the essential items for her child, just to point out where her priorities were. I took the receipt back to the diaper section and using the SKU (the description cut off the diaper size), I found the diapers she bought. Huggies Size 2.

Quickly called my wife and asked her if the woman in her office unattended had a kid that could be in size 2 diapers. You bet she did. So now we had an idea of who the culprit was.

As I left Walmart, guess what I got. Another alert!!! $747.95 at Boost Mobile. Quickly pull up Google Maps and navigate to nearest Boost Mobile store. Run in and the store was empty. No Customers. Ask the guy behind the counter if someone bought a phone in the last 6 minutes. He says nope but he tells me there is another Boost Mobile store nearby and to check with them. I quickly navigate to that store and when I get in the store, there is a woman at the counter with a bag of stuff that looks like it has been rung out already and they are working on something else. I can’t get a good picture of her without being obvious because of the layout of the store, so I decide to do a Facetime video chat with my wife who is now at the local police station with an officer filling out a police report.

I walk outside to start the Facetime and tell them what I am about to do. The officer tells me not to approach her and I tell him to go fly a kite.

I tell them both to be quiet because I can’t figure out how to mute their audio. I walk back in the store and act like I am looking at some phone cases while awkwardly holding my phone so the camera is pointing in her direction. My wife isn’t good at following directions because a minute or so into it I hear her say “Oh my god, that is her!”

Thankfully she didn’t hear my wife because the clerk was talking her through setting up voicemail on the phone. I walk outside and ask the cop my wife is with what I should do. He tells me to try to grab a photo of her and call 911 to get some officers there ASAP.

I walk outside to call 911. As I walk out, the clerk tells me he will be with me as soon as he is done activating her phones and I told him to take his time as I was waiting for someone (the 5-0!!). The 911 operator questioned how I knew it was this specific person and it was hard to put into a coherent thought because I had adrenaline shooting out my eyeballs. As I was on the phone with 911, another alert from Chase popped up for $545.59 at Boost Mobile again. I told 911 that I am sure it is her because of the alerts and hurry up because I think she is about to be done and leave.

I went back into the store to look like I was waiting because I was planning to block the door and not let her leave if she finished before the cops showed up. Officers showed up 18 minutes later. Yes 18 Minutes.

Thank god it takes forever to activate a cell phone.

She was arrested on the spot after she pulled my wife’s wallet out of her purse. She had ‘moved’ all of her stuff into my wife’s wallet but still had all of my wife’s credit cards and her ID in there too. She tried to give the cop my wife’s ID when he asked for ID and the credit card she just used. Maybe from 100 yards away they look similar, but at 3 feet, not even close. She finally told the cop she found the credit card and she could just return the stuff and go on her way when the cop said the ID didn’t look like her.

She seem shocked when the officer said “You are under arrest” and pleaded that she could just return the purchased goods and go home, no harm no foul. In all, this girl charged $2,075.05 in about an hour and 15 minutes. Chase was very good and reversed all of the charges that day and overnighted us new cards. The girl sat in jail for 2 months because bail was set pretty high ($30k) for a crime like this because she has open warrants for her arrest in California for the same exact crime. She is a professional scumbag.

She eventually pled guilty to a lesser charge (still a felony though) and was released on 3 years probation and time served. I keep tabs on her in our County’s online court docket because she owes us $132.14 in restitution for the stuff she tossed and our costs for having to order new checks, etc. Her probation officer has filed a motion to revoke her probation three times, she has been arrested for stealing a few hundred dollars of stuff from Target less than a month after getting out of jail, she failed to show for her court date on the Target thing and a warrant was issued for her arrest and just 10 days later she crashed her car texting while driving with her months old child in the car and was arrested because of the outstanding warrant from the Target thing.

Just a real winner of a contributor to society. If anyone wants pictures, I have plenty to share!!

[Edited by Jim to put in paragraphs to make it easier to read]

Mike… this is the most insane story I’ve ever heard. Thank you for sharing it but this is incredible!

Karen says

Wow! I wonder if I can do this on all of my cards. This is an excellent tip. Glad I read this.

Some have minimums of $1 but every credit card I own will offer email or text notifications.

Marsha says

Hi….liked your story on card alerts. My Chase visa card was recently transferred by Chase to a Barclay’s Mastercard. I had the same alerts from Chase….loved them. So I set up alerts with Barclay’s for email. These alerts take minimum of 24 hours to receive and they do not show vendor…only the amount so you have to remember all charges. I called Barclay’s customer service and was told notifications are sent right after charge is made. No idea why emails are taking so long. Am thinking to go back to Chase. Any advice?

That’s weird that Barclays would say they send them immediately but don’t reach you for 24 hours – if that’s a deal breaker, consider moving for sure!