Vanguard Personal Advisor

Strengths

- Complimentary consultation & plan

- Low management fee (0.30%-.40%)

- Uses low cost Vanguard funds

Weaknesses

- Plans only offer Vanguard funds

Paid non-client promotion. WalletHacks.com receives compensation when a reader provides personal information to Vanguard after clicking the “Vanguard Personal Advisor” links on this page.

When it comes to Vanguard, it’s no secret I’m a fan. One of my first brokerage accounts was with Vanguard, back in 1998, and I could thank my dad for telling me about them (and the Roth IRA!).

So when I say I’ve been a long-time Vanguard investor, I mean it.

And as someone who has been with Vanguard for a long time, I knew they offered financial planning for high net worth individuals. But did you know they offer more personalized help for folks with more modest account balances? They do.

It’s called Vanguard Personal Advisor. If you want to know what it’s all about, read on for our review of Vanguard Personal Advisor.

Table of Contents

Who is Vanguard?

If you’re new to investing, Vanguard may not hold a special place in your heart (it holds one in mine).

Vanguard was founded in 1975 by Jack Bogle, considered the grandfather of the index fund, with an eye towards making investing more accessible to the average family. Jack Bogle absolutely changed the investing game by offering low-cost funds that infuriated his competitors. To this point, there was even a lawsuit in 2015 that argued Vanguard was charging too little!

They’re headquartered in Malvern, PA and as of August 2019, Vanguard has $5.6 trillion in assets under management with over 30 million investors.

I’ve been using Vanguard for as long as I’ve been investing because my father told me about them.

How did he know about them? Because they’re fantastically inexpensive. If you’re a buy and hold investor, you want your costs to be as cheap as possible.

My dad loves them because they are cheap. I love Vanguard because they’re cheap.

How cheap?

Get this — the Vanguard Total Stock Market Index Fund (VTSAX) has an expense ratio of 0.04%. For every $10,000 you invest in VTSAX, you pay $4 in fees. FOUR DOLLARS.

You can see why other brokers were upset. Vanguard wasn’t that cheap back when Bogle founded the company but they were still probably one of the cheapest options out there.

Vanguard Voyager and Flagship

If you’re familiar with Vanguard, you might know that they have various tiers of account types based on your balance.

The first named tier, which happens at $50,000, is called Voyager. At this level, you get to ask for guidance from investment professionals. It’s pretty basic.

The next tier is at $500,000 and is named Voyager Select. At this level, you get a team of investment professionals who can help answer questions, make transactions, and help you out but it’s not a one on one relationship.

The next major tier is when your assets reach $1 million and it’s known as Flagship. With Flagship, you get to enjoy Flagship Services. You can have access to personalized services, investment management, and other specialists.

Vanguard Personal Advisor sits at the first tier – Voyager. This means that with just $50,000 to invest (which is a LOT, but just wait until you see what you get) you can get personalized advice. More on this now.

What is Vanguard Personal Advisor?

Vanguard Personal Advisor (PAS) is their advisory service for investors who have at least $50,000 in assets to invest.

The investments can be in any kind of taxable brokerage account (mutual fund or brokerage), IRA, or trust account. They can’t manage 401(k) and 403(b) accounts, i401(k) accounts, 529 accounts, UGMA or UTMA accounts, and any other investments outside of Vanguard.

So, if you have $50,000 in investable assets that you’d like to put with Vanguard, the service is very straightforward. You start by filling out a form on the site that can help your advisor come up with a plan. You will want to collect some information about yourself to make this as valuable as possible. This includes your income and spending, information about your assets in different accounts, as well as an estimate of your Social Security benefits.

You will also need to try to project forward to understand your financial needs in the future. Maybe it’s paying for your kid’s college or buying a second home or some other financial need. This will help the advisor know your future goals, the timeframe for each milestone as well as your overall plan. You will discuss these during the initial call with your advisor. This call is used with your information to craft a customized financial plan and the plan takes a few weeks to put together.

After they are done, you meet (virtually) with your advisor once again to go through the plan and make any adjustments.

It is only at this point that you have to decide if you want to use Vanguard Personal Advisor.

That’s right — the initial call, the building of the customized plan, and the call afterward to make adjustments to that plan – no obligation whatsoever. If you decide you’d rather do this yourself, you can.

Here’s a quick video breaking it down:

Reader Experiences with Vanguard PAS

I know a few folks who went through the process of using Vanguard Personal Advisor and had a chance to interview them all to collect a more hands-on report of what it was like.

As a whole, they all agreed that it was a fairly straight forward process that progressed very quickly. Each one submitted their information, had the initial meeting, waited about two weeks, and were given various scenarios to select from. A few of them went forward and invested in the proper funds (more accurately, most simply re-allocated their existing Vanguard funds) while others decided to handle it for themselves. No one who decided against using PAS felt that their advisor reacted negatively.

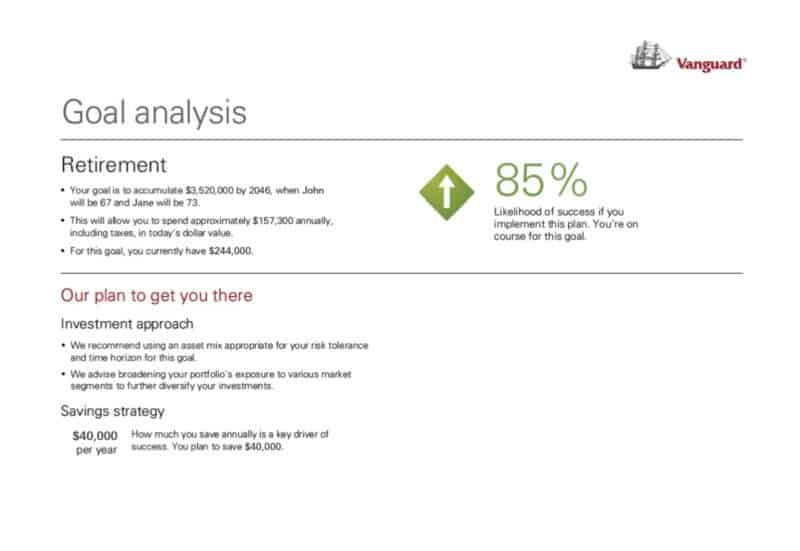

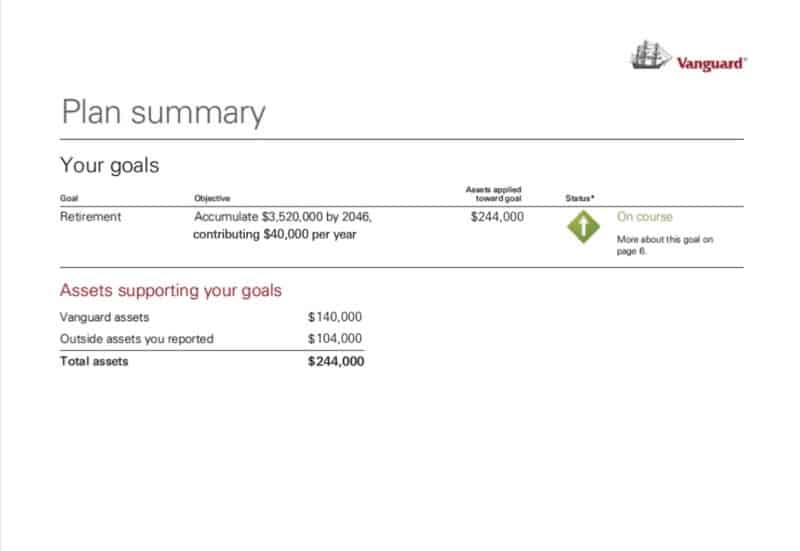

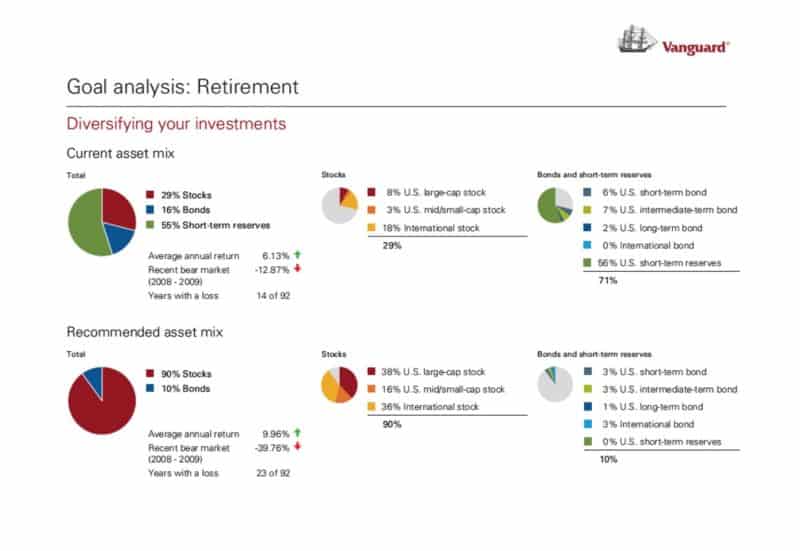

One reader, Michael, said that the process seemed very rudimentary and there was more “give and take and discussion with the financial planner.” The financial planner was the initial call where they confirm your information, challenge some of your assumptions, and then asked you about future funding needs like your “travel plans, large gifts you want to make, car purchase habits, etc.” He received his scenarios about two weeks after this call. I didn’t see his plan but it was similar to the example plan below (the percentages and funds would be slightly different).

The Financial Plan

The financial plan they produce isn’t super complicated and consists of a series of Vanguard funds to help you reach your goals. They share a sample plan on their website that includes the following pages:

The plan itself contains how much of each asset class you need and each asset class generally only has a few Vanguard funds included. If you have funds there already, this plan will help you reallocate them into the appropriate areas.

What’s nice is that investing in Vanguard funds doesn’t cost you anything. You can buy and sells shares of their mutual funds and ETFs. The only cost is if the fund has a purchase or redemption fee plus the expense ratio. They’ve always been one of the most inexpensive investment options available and the PAS is just a layer on top of it.

How Much Does Vanguard Personal Advisor Cost?

Unlike many traditional financial advisors, Vanguard Personal Advisor advisors aren’t paid a commission. They don’t get anything for pitching Vanguard products and you don’t pay an hourly fee. (in fact, that initial phone call is complimentary with no obligation)

The fee structure is based on whether you are doing an all-index investment option, active and index investment option, or an ESG investment option.

For Vanguard charges just 0.30% of the assets they manage on assets up to $5,000,000. The percentage fee that is assessed on your assets is lower on higher balances, based on this schedule:

| Managed Assets | Fee |

|---|---|

| On assets up to $5 million | 0.30% |

| On assets above $5 million and up to $10 million | 0.20% |

| On assets above $10 million and up to $25 million | 0.10% |

| On assets above $25 million | 0.05% |

So the first five million pays 0.30% and then the next five million pays just 0.20%. This means that if you had $6 million in assets under management, you’d pay a $4,250 quarterly fee or 0.28%.

If you want a mix of index and active, the price only goes up to 0.35%.

How does this compare with other services?

Fidelity Portfolio Advisory Services

Fidelity offers a Portfolio Advisory Services Account that has professional investment management through an advisor. It has two levels of service.

The first, for investments of $50,000 to $250,000, you get access to a team of advisors that work with you. They will help you establish goals, track your progress, and perform annual reviews. The advisory fee for this service is 1.50%.

The next tier is for investments greater than $250,000 and that gets you a dedicated advisor through their Wealth Management offering. This is a more detailed service and similar to what Vanguard offers with Personal Advisor. The advisory fee is anywhere from 0.50% to 1.50% depending on the site of your investment.

Betterment Roboadvisor

Betterment is a roboadvisor that charges a flat 0.25% fee for their Digital service and 0.40% on their Premium service. The Premium service is the one that gets you access to in-depth advice of your non-Betterment investments and unlimited access to their CFP professionals.

It’s important to note that Betterment is a roboadvisor whereas Vanguard PAS is an advisory service where you partner with an advisor to come up with a plan and they send you a quarterly update. If you’d like to meet with them on that schedule, you can. If you don’t have to, you don’t have to meet up on a quarterly basis. Betterment and Vanguard PAS are not substitutes but I felt a comparison of their fees was fair.

Vanguard’s PAS compares quite favorably to one of their biggest competitors, Fidelity, and one of the biggest roboadvisors, Betterment.

Conclusion

I’m at a point in my financial development that I prefer to manage my own investments so this isn’t a service that appeals to me at this moment. However, I see value in speaking with one of their Vanguard Personal Advisor advisors just to see what they say. Having them help you come up with a plan, tailored to the financial needs you have, seems like a smart idea.

At worst, you spend a few hours speaking to someone to get a financial plan you can implement yourself. With no obligation, it seems like an easy way to find out if the service could work for you and if it doesn’t, you get a great financial plan out of it.

If you like what you hear and you want to work with someone, paying 0.30% is a fraction of what you’d pay a human advisor and is even less than their competitors like Fidelity and Betterment. Vanguard has long been known to be a very affordable investment option and the Personal Advisor Service seems to keep with that mission.

Find out more about Vanguard Personal Advisor

Disclosures: All investing is subject to risk, including the possible loss of the money you invest.

For more information about Vanguard funds and ETFs, visit vanguard.com to obtain a prospectus or, if available, a summary prospectus. Investment objectives, risks, charges, expenses, and other important information about a fund are contained in the prospectus; read and consider it carefully before investing.

Vanguard Personal Advisor are provided by Vanguard Advisers, Inc., a registered investment advisor, or by Vanguard National Trust Company, a federally chartered, limited purpose trust company. VAI is a subsidiary of VGI and an affiliate of VMC. Neither VAI nor its affiliates guarantee profits or protection from losses.

The services provided to clients who elect to receive ongoing advice will vary based upon the amount of assets in a portfolio. Please review the Form CRS and Vanguard Personal Advisor Brochure for important details about the service, including its asset based service levels and fee breakpoints.

Vanguard Marketing Corporation, Distributor.

All ratings as of March 14, 2022, based on review of services offered during calendar year 2021.