Do you know how many tax allowances you are allowed?

When was the last time you filled out a Form W-4?

If you were like me, and many other employees, you filled it out when you were hired and probably never thought about it since.

The Form W-4 is what determines how much of your salary is withheld for taxes. Your employer requires you to fill out this form but rarely asks you whether it needs to be updated.

Tax law seems to change every year. Your life situation likely changes every year.

You should be updating this whenever there is a major change.

Most recently, one of the biggest changes to tax law happened a few years ago with The Tax Cuts and Jobs Act of 2017. It roughly doubled the standard deduction, “preventing” millions of taxpayers from itemizing their deductions. It also eliminated personal exemptions, which were one of the main factors determining tax allowances claimed.

It can get confusing so today we’re going to try to clear it up for you!

Table of Contents

🔃Updated February 2023 with the latest tax numbers for 2023.

What Are Tax Allowances?

Tax allowances are approximate estimates of reductions in your taxable income for federal withholding tax purposes. When you get a new job, as well as at the beginning of each new year thereafter, you complete an IRS W-4 form: “Employee Withholding Certificate”. This enables your employer to adjust your taxable income which will, more closely, determine the proper amount of income taxes to withhold.

The more allowances you claim, the less your employer withholds from your paycheck for taxes.

If you get your withholding allowances right, the amount of federal income tax withheld will come very close to your actual tax liability for the year. No free loans to the government!

In a perfect world, you’ll neither owe, nor be entitled to a refund after filing your tax return. Owing the IRS money is never an optimal outcome; not only because of the actual tax liability, but also because of the potential penalties and interest.

While most people prefer getting a refund, it’s really nothing more than a return of your own money. If you over-withhold, which is really what creates the refund situation, you’ve effectively given the IRS an interest-free loan. What’s more, it’s money you could have earned interest on yourself but didn’t.

There are various tax filing scenarios that may apply to you. You want to try to determine how many of these tax allowances you should take in the coming year.

If You Have Income and Someone Else Can Claim You as a Dependent

The best strategy (if this is your filing status) is to claim zero allowances.

This will mean that your employer will withhold the maximum amount of taxes each paycheck and you’ll get a refund at tax time. This is the safest option when you are a qualified dependent.

Single Filers and Heads of Households

As a single filer with a single primary source of income, claiming one tax allowance should be sufficient.

It will either result in a small refund or a small tax liability. As much as you try, it’ll be close to impossible to have your federal withholding tax match your actual tax liability exactly.

However, if you expect to be able to itemize deductions – which means your deductions will exceed the $13,850 standard deduction for 2023 – you may want to consider claiming additional tax allowances. To do this properly, you’ll need to make a reasonable estimate of the excess of your itemized deductions over your standard deduction.

If you work two jobs throughout the year, split your allowances between the two jobs. For example, if you claim two tax allowances, you should take one for each job. If you only take one tax allowance, take it on the job that pays the most money.

If you’re single and have at least one dependent child, you can file as head of household. If you have one or more children who you can claim as a dependent on your tax return, you can add one additional tax allowance per child. For example, if you’re filing as head of household with two qualifying dependent children, you can probably claim a total of three tax allowances on your W-4.

Once again, there is no personal exemption, but the additional tax allowance will accommodate the lower tax liability that you’ll have if you can claim the child tax credit. This can reduce your income tax liability by up to $2,000 per qualifying child.

Naturally, if you don’t have any qualifying children, you shouldn’t take the additional tax allowance. Also, be aware that the child tax credit phases out if your income exceeds $200,000.

Married Couple Filing Jointly

If you’re a married couple filing jointly, you should claim one tax allowance for each of you. If you have dependent children who qualify for the child tax credit, you can add one additional tax allowance for each child. The child tax credit phases out with an income of $400,000 or more for a married couple filing jointly. If your income exceeds this amount, you won’t be able to claim the credit, nor take the additional tax allowances.

Just as in the case with single filers, you may be able to take even more tax allowances if you’re able to itemize deductions.

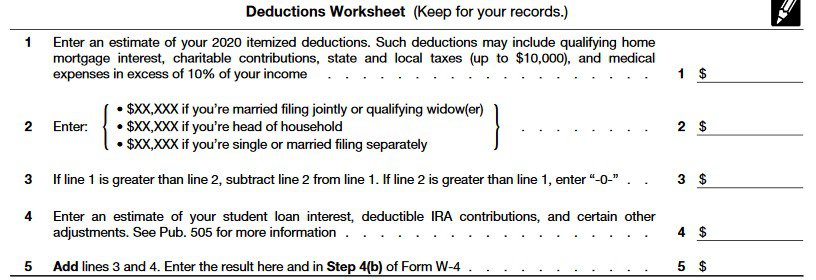

The IRS even provides a deductions worksheet with your W-4 form to estimate the impact of your itemized deductions on your tax allowances for the coming year. This form can be used if you are married filing jointly, single, or head of household.

On Line 2 where you see $XX,XXX, the amounts that should appear in those X’s are $27,700 if you’re married filing jointly or a qualifying widow(er), $20,800 if you’re a head of household, and $13,850 if you’re single. These are the standard deductions for 2023.

Notice that Line 4 provides for an estimate of your student loan interest, deductible IRA contributions, and certain other adjustments. You can use this line to reflect tax-deductible contributions to an IRA, a Health Savings Account, alimony and certain other “above the line deductions.”

The net amount shown on Line 5 will carry to the first page of the W-4 and increase the total tax allowance you’ll be claiming for the year.

Other Complications that May Affect Your Tax Allowances

So far, we’ve been discussing the number of tax allowances to claim if 1) your income is derived primarily from your job, 2) you itemize your deductions or take the standard deduction, or 3) if you have dependent children who qualify for the child tax credit. However, there are other situations that can affect your tax allowances that fall outside those general categories.

One is investment income. If you have a substantial amount of investment income, you may want to claim fewer tax allowances or none at all. Any taxable investment income will increase your tax liability. Unless you’re making estimated tax payments to cover the liability of the additional income, you may want to do it through higher withholdings from your regular job. You can accomplish this with fewer tax allowances.

Another potential situation is having a side business. Let’s say that in addition to your regular job you also have a side business that earns additional money. Technically speaking, you should be setting up quarterly tax estimates to cover the tax liability on that income. This is especially important since self-employment income is also subject to the self-employment tax which is about 15.3% by itself.

If the income you receive from your side business is expected to be just a few thousand dollars for the year, you may want to decrease your tax allowances rather than making estimated tax payments.

It’s also possible your business is turning a loss. If it is, you may be able to increase your tax allowances.

Still, another example is real estate or partnership income. Either can have an impact very similar to a side business.

When in Doubt, Hire a Professional to Help

If you have any of the above situations, the best strategy may be to discuss it with a professional tax preparer. The calculations can get complicated, particularly for someone who doesn’t prepare income taxes on a regular basis.

It’s better to pay a tax preparer to give you a close approximation of your actual tax liability and the number of tax allowances you should claim than leaving it to chance. An unexpectedly large tax liability could add interest and penalties to an already large tax bill.

A tax professional can tell you if you’re able to increase tax allowances due to business losses or if you’ll need to make estimated tax payments for business or investment income.

Leave a Comment: