The first credit card I ever got was an AT&T Universal Card because someone had a table outside Doherty Hall at Carnegie Mellon University, my alma mater. I may have gotten a t-shirt out of it too.

The biggest appeal of the card? How I could get one as a freshman with no income (the guy told me to put my tuition for a salary… I’m pretty sure that wasn’t legit).

Fast forward a million years and I no longer have that card (it no longer exists, but for a while, you could still see an application page for it and its fantastic offer of 35 cents per minute domestic calls!) and instead use a series of three cards depending on the situation. All told, our total “credit limit” across every card (several of which are in the desk drawer) is over a hundred thousand dollars.

How did we get that much credit? Simple. We just asked for more.

And kept asking. And asking.

You can get more credit too, all you have to do is ask!

Why would you do this? It can improve your credit score. Credit utilization is a major factor in your credit score and credit utilization is a simple math calculation – total credit used divided by total credit available. When you increase your credit limit, you are increasing your total credit… thus lowering utilization.

There are three ways you can get your credit card to increase your credit limit:

- Wait – As you demonstrate that you can use and pay off credit, card issuers will increase it automatically. But you’re not the type to wait around for things to happen, so let’s talk about the other two.

- Ask via telephone – Call the customer service number on the back and navigate your way to a human being. Then ask about the process for increasing your credit limit without a credit inquiry. This is always an option but I’ve never actually done this myself because you can also…

- Ask online – Almost every credit card issuer has a way to request a credit line increase online. Customer service representatives in a call center cost money, computers do not. This is the way I’ve always done it and this is what I recommend. You can get a credit line increase faster than you can reach a human being on the telephone.

When doing this online, and on the phone but it’s less obvious, you want to get the increase without a credit report request. When it doubt, especially on the phone, ask if the increase request will require a credit review. If it does, don’t submit the request. If you don’t know, don’t submit the request. Better safe than sorry.

We include screenshots for Citi, CapitalOne, and American Express below but each issuer follows the same basic flow. Find your credit management area of the account and look for Request Credit Limit Increase. On the request page, confirm that the issuer will not initiate an inquiry with your credit bureau or request your credit report.

This is very important.

You should look for language like “instant approval” or “automatic” – which means a computer will have made the decision based the numbers they have in front of them. If it requires a manual review or a credit check, stop. That hard inquiry will more than negate the positive effects of an increase.

If in doubt, don’t make the request.

Table of Contents

🔃 UPDATED: Updated January 2024 with new screenshots and process flows for requesting a credit limit increase from Chase. For some time, perhaps just because of the pandemic, Chase required you to call in to make an increase.

Citi

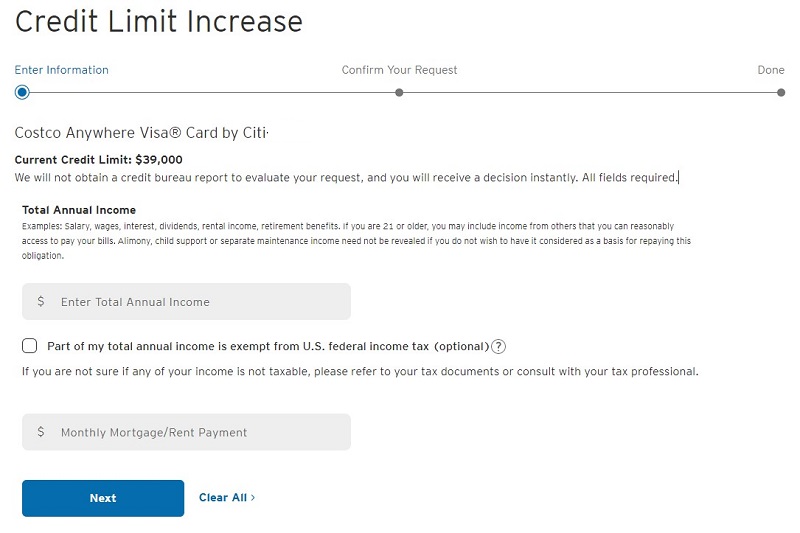

Log into your account and click on Services in the top menu and then click Credit Card Services.

On the next page, look in the left column titled Card Management and “Request a Credit Limit Increase” will be third from the bottom.

As you can see, it says “We will not obtain a credit bureau report to evaluate your request, and you will receive a decision instantly. All fields required.”

For Citi, you don’t even need to enter in the amount you want. Just enter your annual income, your housing payment, confirm, and boom!

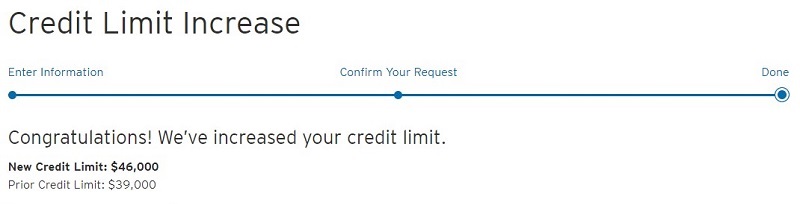

It took 10 seconds and my credit limit went from $39,000 to $46,000 with no credit pull. A 17.90% increase in the limit of my card with no risk involved.

I could ask for more but it would require a credit review, which includes a credit report hard inquiry, which would decrease my score.

I don’t need the credit limit for the limit (and at $46,000 of limit, I never come close to hitting this among all my cards let alone a single one!), so I stop.

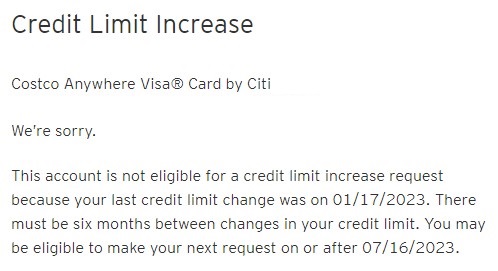

With Citi, you must wait at least six months between each request. Since this last request was made on January 17th, 2023, I have to wait until July 16th to ask again. Fortunately, Citi will tell you this!

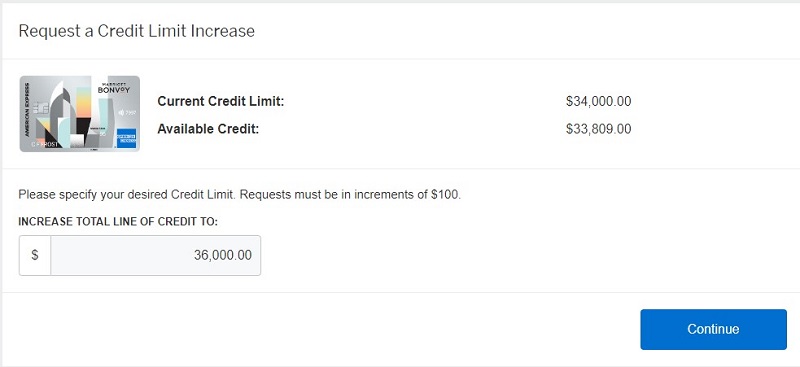

Capital One

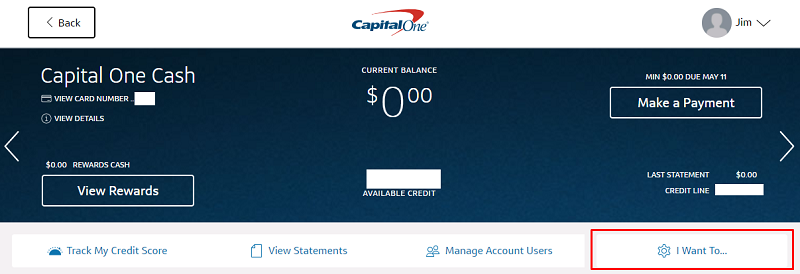

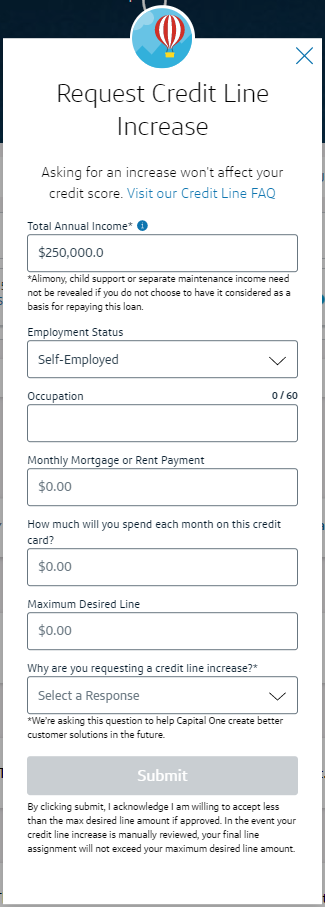

Log into your account and select your card, then find the Gear Icon and “I Want To…” menu item:

In the next menu, look in the lower left for Offers and Upgrades group, you’ll see Request Credit Line Increase – click that. This is the form that will pop up:

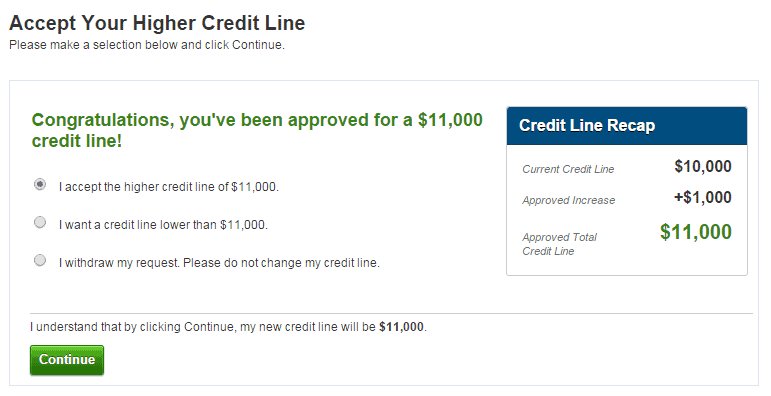

In May 2021, I had a limit of $11,000 with this card but I hadn’t been using it. I requested a $2,000 increase and claimed I’d use it for $4,000 in spending. Sometimes the approval is instant, sometimes it needs a review.

In my case, I saw the needs to be reviewed (I will check my credit report to see what kind of inquiry popped up and update this post):

In the past, if you were instantly approved, it would show this screen:

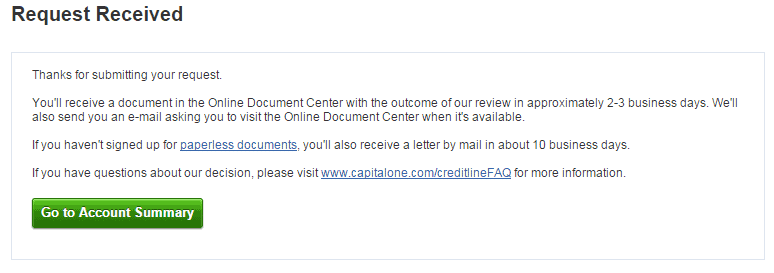

I submitted my information, confirmed on the subsequent page (not shown), and boom!

A $1,000 increase on a $10,000 credit limit, increasing my credit line by 10%.

If those were my only two credit cards, my total credit would’ve increased from $26,000 to $29,200. For thirty seconds of work, I’ve increased my total limits by $3200 (+12.3%).

In this most recent request, in May 2021, my request was declined because:

- Recent usage of this account for monthly spend has been too low

- Recent use of this account’s existing credit line has been too low

Both are fair reasons because I have not been using this card – smart! Make sure you use the card before requesting an increase because some issuers are using that in their determination.

I have yet to request an increase because this card isn’t in our regular rotation.

Chase

For years (perhaps because of the pandemic), Chase required you to call in to request an increase but now it appears they have reinstituted the online form!

To find the menu item, click onto the card you want to reveal the card details. Then look for the “More” menu item. Click it and look for Account Services, the Request credit limit increase item is located there.

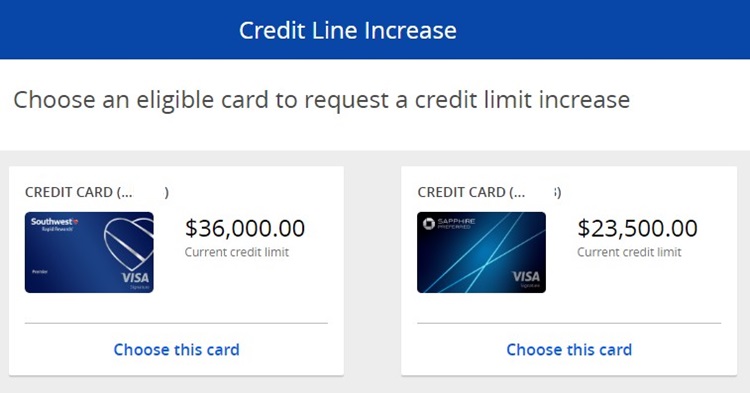

From there, you are asked to pick which card you want to increase:

Pick one and you’ll be asked to update your Total gross annual income and your Monthly mortgage/rent. Once you enter that, you’ll be asked to confirm your entries. Once you click submit, you’ll see a “we’re working on it” type of screen.

Then, you’ll either be offered an increase, declined, or what I saw:

American Express

I was unable to find the link to the credit limit increase form through their new menu navigation but on this FAQ page for how do I request a credit limit increase, they link to this form. The FAQ page appears to be for the UK but when I’m logged into my account, it shows the proper page for the US.

You’re asked for total annual income and assets (optional) and then they ask you to connect your bank or upload your three most recent bank statements to confirm your income.

We didn’t go through this but I suspect the answer is rendered on the next page (or after a brief human review).

Rejections & Further Review

Sometimes your request will not be automatically accepted, this will happen if you requested and were granted an increase recently. “Recently” could be as few as six months or as long as 18 months, it depends on the issuer’s practices.

In this case, Capital One will not increase an account that’s less than 3 months old or received a credit line increase or decrease in the last six months.

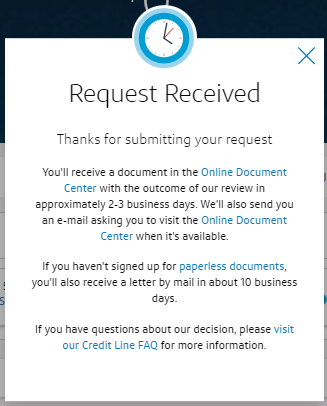

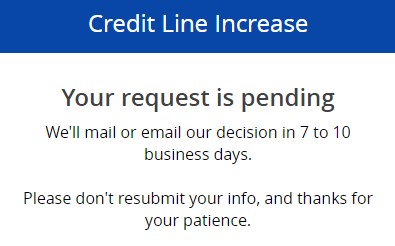

With the American Express walkthrough, I was actually given a “further review” notice. I requested a 10% increase to my credit limit and was given this message:

Your request for a line of credit increase has been submitted.

You will receive a written response within 7-10 days.

But there’s no cost, except your time, to asking and not getting the increase.

How often can I do this? It depends on the issuer but most will only approve increases every six months. They will also require you to have a card for more than a few months, sometimes as little as 60 days. They just granted you a line of credit based on your application, they want to see how you behave with it before making a decision on giving you more. Each issuer will answer this question in a FAQ on their site.

There are some folks who request an increase every 6 months like clockwork. I’m not nearly that diligent, I ask when I remember and that usually works out to be once a year for the cards we use regularly and never for the ones we don’t.

If you want to do this regularly, I recommend creating a calendar notification that reminds you every six months to request an increase.

Over time, your limit will creep up and then you too can live the American Dream of having way more credit than you need. (which could be important if we move towards a cashless society!)

What happens if they do make an inquiry? If it’s a hard inquiry, expect a single-digit fall in your credit score for about 12 months. It’s as if you just applied for a new credit card. Hard inquiries will cost you a few points but the impact subsides after a year. The higher your credit is now, the bigger the dip.

(and if you ever check your report and see suspicious inquiries, know that you can get hard inquiries removed for several reasons)

If you haven’t asked for an increase in the last six months, I urge you to try now and report back what you find!

Have you done this?

What’s your total credit limit and what’s your system?

Kevin says

When I tried to do it online, my Bank of America Royal Caribbean card said very specifically that it would run a credit report before increasing my limit. What can I do to increase my limit without hurting my credit score?

Ahhh, that stinks. They may not have a system for automatic increases OR it was increased within the last X months (sometimes X is 6 or 12) and so automatic increases are off the table.

I would try calling them and asking if there’s a way to review it for an increase without a credit inquiry, that’s the only option available to you. When they do, I recommend asking them what the process is so you know for next time (and let us know!) It could be they don’t do automatic increases at all!

Tony says

Bank of America sucks. They are one of the few credit card providers that will not give you a credit line increase without doing a hard pull. And even after the hard pull, they will increase by only $2000 or less which is not worth the effort. I was able to get increases of $5000 on Discover and Chase without credit pulls.

Shaun says

Wow! You really know what you’re talking about. Citibank just increased my credit limit from $6000 to $7200 instantly. One of my Capital One accounts gave me an increase of $1000 the other Capital One account said it’s under review and they will be in touch in a few days . All of this was done with no credit check and in only a few minutes. Awesome tip!

Once you know the rules of the game, it gets much easier right?

Just don’t carry a balance! They give you more credit for a reason – you’re creditworthy, they believe you’ll pay it back, so they give you more. Just don’t fall into the trap of accruing debt and paying their absurd interest rates.

Marcos says

I just tried this tick on 2 credit cards, Citi and a Capital One. I was instantly approved for an $1100 and $500 dollar increase. Thanks for the tip Jim!

Heeey there you go! Now just wait six months and you can probably do it again. 🙂

John says

Chase require a hard pull for a credit increase. I have tried when calling them a few times for it =\

Then wait a couple months and try again, if you call they’ll still need to do a hard pull (which you don’t want).

Darvin says

Chase will always require a hard pull.

Bank of America – will always require a hard pull.

USAA – will always require a hard pull.

CITI – you can request for an increase every 6 months and it will be soft pull.

AMEX – you can request for an increase every 6 months and it will be soft pull. You can request up to 3 time your current credit limit. But cannot be more than $25K

Discover – you can request for an increase anytime, but you are better off requesting every 6 months, and it will be a soft pull.

Mr Jones says

Do you know which issuers let you do it over the phone (without talking to a person?)

I’ve never tried to do it over the phone, why would you want to do that instead of via the web?

Mike says

It might be necessary to do via phone not web.

I just called Best Buy, after not being able to do it online.

The first person I spoke to said it was not possible. I was skeptical.

I called back and spoke to another person, who said it was possible, and walked me through the process without requesting a hard pull.

Just to answer your question of “why would you want to do that instead of via the web?” 🙂

Good experience, thank you for sharing Mike!

Jennifer says

Hi Jim,

I just opened my american express credit card account last week. I have a fraud alert on my credit file so will that make them do a hard inquiry every time? When should i apply for credit limit increase next 90 days or 6 months? Thanks for you time!

When you open a new credit card, it’s always a hard inquiry.

You will likely need to wait 6 months on a new card before asking.

Tami says

Hi Jennifer,

I’ve had my Amex for 1 month now. I called to inquire on when I can request an increase. They said I may 60 days from my opening date. From my understanding Amex allow you an initial request within 90 days from opening the account. Then every 6 months after. Call to double check. Hope this helps!

Taylor Blessing says

Just got that exact message from Amex, was yours good or bad news? seeing a lot of conflicting answers from different sites.

It depends on whether they approve the limit. 🙂

Mark says

After reading this, I followed the steps and got a $1500 increase on each of 2 cards with Citi. six weeks ago, I increased with Chase over the phone. They said they’d need to place a hard pull but so far it hasn’t showed up on TransUnion or Equifax reports. I don’t think they actually did one. I opened 2 brand new BofA cards six months ago and they never did a hard inquiry.

william says

all my credit cards are maxed out but never misse a payment and my score is a 700 you think i should ask for increse so my balances will be less then 30 percent

I doubt you’d be able to get your utilization under 30% but asking for an increase could help your score.

A bigger issue is that you’ve maxxed out your credit cards in the first place. Have you looked into ways to paying down your debt so it’s at a lower level?

Jennifer says

I got a credit increase 2x the link it I had ( cl $1,000 increased to $3,000) you only have to wait 62 days after opening your card per the American Express rep/ agent! Amen it #1 in my opinion in customer service. I love the amex manage your online account. So just fyi, you don’t have to wait 6 months after opening an American Express account Jim

Jennifer says

Sorry misspelling is auto reply on my mobile device ?

Wayne says

Does anyone have a positive or negative experience asking for a credit increase on a card that has not been used in a few years? It is a Capital One. I use other cards for my expenses. Or should I make a few purchases on the card and ask 6 months later?

I tried this yesterday (specifically with a Capital One card too) and was denied because I didn’t have any activity to make a determination. So you need activity before they’ll increase it.

Wayne says

Thanks for the input before trying. I might try charging a few hundred a month and ask 6 months from now.

To be honest, I was surprised to get the answer I did! I’m glad I saved you some time!

chris says

I have a capital one venture rewards that i use for business expenses of sometimes $2-$3k/mo and then immediately paid off. Had it 6months. Never late. Score is 700 with 0% utilization. Had $5k SL and with this tip just requested thru app and got an ADDITIONAL $5k! Now at $10k total and will probably ask again Jan 2019. Thanks for the tip!

rajesh says

Hi,

I have two Amex credit cards opened in 1 week gap, can i request credit limit increase for both cards when i reach 61 days mark.

The request waiting period is linked to the individual card, not your account.

Nova Skyy says

Jim,

You are awesome!!! I’m in the process of paying down all of my credit cards and I’ve noticed that two of my credit limits were increased without asking. I will wait 6 months to inquire for an increase. I did however make a rookie mistake. In the process of paying down my cards, I did cancel some cards with balances that I continue to pay on. Should I ask to reopen my card or will this cause and hit on my report?

I would call and ask how they would do that – if they closed it and are just giving you a new account, that’s bad. Not only did you lose the account’s age on your average but you’ll now add a fresh new account. If they’re able to re-open the recently cancelled (which feels unlikely), then that would be beneficial.

M. Ramsey says

Hi Jim,

You seem to be a wealth of information so my question is I’ve gotten several upgrades from store cards to Store/Mastercard (ie Wal-Mart, Target, Nordstrom, etc) Is this good or bad and do/will I lose my history established with store card?

If it’s still a store card, you won’t lose history because it’s part of the same account.

Christopher Winters says

I have two Capital One Cards, and I only receive $500 increases for several years now. Is there any way to get the increase higher than that? I don’t know the formula these companies use to grant higher increases. Should I indicate less money that I pay for rent/mortgage? Should I indicate that I spend a lot on all my credit cards? On this credit card?

Jen says

Have two long-standing accounts with BB&T with $2500 limits each.

One has a zero balance and the other has a $300 balance.

How much of an increase should I ask for on each card?

806 credit score, no late payments ever

Personally, I’d probably ask for an increase to $3,000 on each and see what happens? I don’t think it’ll impact your score that much though but that depends on the limits of your other cards. Your score seems pretty good as it is (but it never hurts to improve!).

If they don’t automatically grant the increase, and start asking for more information, decline because you don’t want a hard inquiry.